Aviva’s Financial Education Team have seen a significant increase in activity during 2019. They provide presentations to workplace pension members either face to face or by live online streams. These include “Mid-Life MOTs” designed to support the growing population of over-45s in workplace pension schemes. These sessions are run in conjunction with Aviva’s Health business and cover both wealth and wellbeing looking at members’ financial situation and also educating them in matters such as diet and fitness. They also run seminars aimed at members aged over 55 to explain their options in retirement.

Last year the team presented to almost 37,000 of you, an increase of almost 40% on 2018. The IGC has seen one of the team’s presentations and it is delivered in very clear, easy to understand language with key messages covered well. We have chosen this year to provide an example of the type of material Aviva uses to educate members. At Appendix A you can see some material which they use to show the benefit and the true cost to members of increasing their contributions.

The IGC view this service as positive and very valuable – it looks to educate members at key stages of their working life in the importance of saving for a better retirement. It is a constant battle for pension providers to engage effectively with members, and education is a key factor in encouraging members to take action to improve outcomes in later life. Feedback from both members and employers has been very good, with 96% of members feeling motivated to take action as a result of the presentation.

The IGC encourages Aviva to make this offering more widely known to employers so greater numbers of you can benefit from this help. We also feel that Aviva should extend this service to help members under age 45 (e.g. at significant life events such as changing employment) and that more presentations should be available online and on demand (i.e. webinars, films etc.)

Aviva provides a financial advice service which is available to all their pension customers. This service has been repositioned to provide pre-retirement rather than at-retirement advice and also includes a specialist team of advisers dealing with advice on transfers from Defined Benefit (DB) schemes where advice is mandatory for all transfers over £30,000.

Members are only charged for advice after an initial meeting with the adviser and after having signed an agreement. Charges are set at 2.5% of the value of the pension assets transferred which is capped at a maximum charge of £5,000. This is an increase in fees over previous years, but the IGC believes it represents good value when compared to charges levied by other firms and independent advisers.

The IGC has also met the leaders of the advice team to discuss the operational aspects, training, standards and philosophy. The team was also assessed externally and independently, and the results were positive.

The operating principal for the advice team is to cover costs rather than operate as a profit centre for Aviva. The service operates on a non-contingent charging basis, which means once an agreement is signed by the customer, adviser activity is chargeable i.e. the customer will be charged for the personal recommendation whether that is to remain in their DB scheme or to transfer.

A view on whether a transfer is suitable or not is only given when a full analysis of the member’s circumstances, attitude to risk and objectives has been completed. The adviser recommendation is tailored to every member and must pass the ‘clearly’ test (clearly in the member’s best interests).

If following the analysis Aviva cannot offer the best destination outcome, then options will be explained, and the customer will not be charged. Aviva Financial Advisers do not accept transfers against advice given and operates within a robust control framework to ensure this principle is not abused. This includes 100% quality assurance checking which is undertaken independently.

The IGC is satisfied that the service offered represents good value and ensures that members have access to a quality advice service at the right time.

In 2019, we asked Aviva to undertake some research to understand more about the views of younger savers (both “Millennials” and “Generation Z”). More younger members are being enrolled into their employer’s pension scheme as a result of auto-enrolment, and the IGC want to understand more about their views around Value for Money.

Aviva has undertaken an initial survey of their own staff on this topic and encouragingly we found that most of the respondents in both age groups were saving at or close to the maximum personal contribution to their pension to benefit from a higher employer contribution. Not surprisingly, the reasons for not making higher contributions were due to other financial commitments such as saving for a home or paying off debt such as student loans.

We asked what would encourage them to save more, and most respondents felt being nudged into increasing their personal contributions was an excellent way of making them think about their pension more carefully, the caveat being that these shouldn’t be too frequent. A smarter way of providing “what if?” projections to show the impacts of saving more were also highly rated.

One of the more surprising responses was around environmental and socially responsible investment options (‘ESG’) in the scheme default fund. While there was an overwhelming response that this was very important, most said that they would only consider it if returns on investments did not suffer a resulting decrease, and that charges were not higher. This area and views upon it are fast-changing and the IGC expects that these views may alter to some extent in the future. In summary, the research showed that the respondents were generally engaged with their pensions, most pay more than the minimum contribution, they see low cost and a good choice of investments as a key Value for Money driver, and that pension contributions are a priority alongside housing and living costs.

We have asked Aviva to extend this research and they have agreed to undertake a significantly wider research exercise in 2020. More detail of these plans can be found in the section of this report setting out our priorities for the year. The IGC is keen to see results over a larger member sample from different employers and, in particular, to see if views on ESG aspects of investment funds are moving.

Of course, Aviva can only help you manage and engage with your pension if they know where you are! The FCA expects providers to manage their “gone away” population (“address unknown”). Data protection legislation also requires providers to have up to date addresses for their customers.

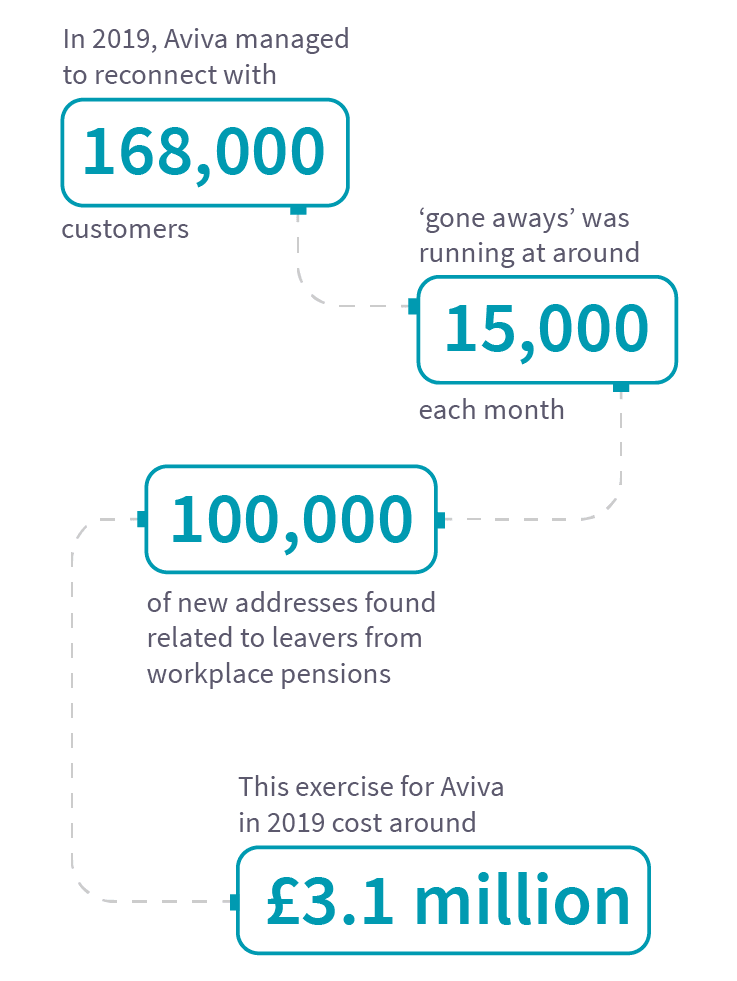

In 2019, Aviva managed to reconnect with 168,000 customers, although new volumes of “gone aways” was running at around 15,000 each month. 100,000 of new addresses found related to leavers from workplace pensions. This exercise for Aviva in 2019 cost around £3.1 million which in our opinion is money well spent.

Aviva is therefore being proactive in their approach to customer tracing. In addition to more traditional methods of tracing customers they are actively engaged with both the Association of British Insurers and the Government to explore better methods of identifying customer addresses. This could be by using alternative data sources such as the DVLA, TV Licencing and HMRC. They believe that this would allow them to trace around 80% of customers for whom they do not hold a current address.

Why is this important to you? Throughout the pensions industry there are billions of pounds of unclaimed assets, including pension funds and death benefits. We are satisfied that Aviva is going further to ensure that they can re-engage with their customers and it will be interesting to see the outcome of their actions in this area.