Aviva has now completed changes to its two main investment default funds. Over a million of you, around a third, invest in these funds and so it is important that they perform well and are subject to good investment governance. A default fund is the fund that your contributions are invested in unless you make specific choices of alternative funds. These default funds are considered to be Aviva’s flagship funds in the pension ranges.

My Future invests in passively managed funds with BlackRock Investment Management Limited being responsible for deciding the allocation between the different types of investments within the funds.

My Future Focus invests in both passively and actively managed funds but with Aviva Investors Multi-Asset investment team being responsible for deciding the allocation between the different types of investments.

In both cases, the allocations to the different types of investments will vary over time depending upon the investment managers’ views on expected future risk and returns.

My Future has a 15-year glidepath, and so if you invest in this fund, Aviva will automatically start to “de-risk” your investments when you are 15 years from retirement. For My Future Focus, the glidepath is 10 years. The difference between the two glide paths arises from the managers’ different views on the expected volatility and returns from the various asset classes. Before you reach your glidepath, you are invested in the “growth” element of the fund which aims to maximise the return on investments whilst minimising the level of investment risk (or volatility) to which your investments are exposed. The assets within the growth fund as at the end of 2019 is shown in the charts below:

Source – Aviva

The IGC has assessed the two default funds and while it is our opinion that both are suitable for longer-term pension savings, we view My Future Focus as providing an overall more attractive investment solution. While the fund is slightly more expensive than My Future, we feel it offers the prospects of better long-term growth due to the more diverse range of investments it uses. It also has a more evolved approach to the integration of the influence of environmental, social and governance (ESG) factors on expected future returns. My Future Focus will cost you 6p more than My Future for every £100 invested which we feel provides Value for Money given the added asset classes We have asked Aviva to tell us what they are doing to promote My Future Focus as a preferred solution in a market that is very price conscious.

Investment governance is important to ensure that the fund you invest in does what it says on the tin. We have attended Aviva’s Investment Governance Committee meetings and seen how they assess funds to ensure that they perform as expected and do not deviate from their stated objectives. In addition, we heard about the process for removing funds that are not achieving their objectives.

Aviva doesn’t only assess their own funds or their “core” fund range. They also look at funds designed by employers and their advisers. If Aviva doesn’t believe that these funds are suitable for members then they simply don’t let them use the Aviva platform. While this is rare it is not unheard of and we have had evidence in previous years where this has happened. In particular, Aviva will no longer allow default fund solutions where the only option is to target an annuity at retirement.

Aviva has removed 24 funds from their investment offering this year for various reasons. For those of you who may have been invested in these funds you will have been written to and asked to switch your investment and, if you didn’t choose an alternative, they will have switched you into an equivalent fund which aims to meet similar objectives to your original choice.

In 2019 the decision was taken to close a number of Invesco funds. These closures will be completed in 2020. In addition, as part of the ongoing governance of their own funds, Aviva has worked with the manager of one of its largest funds to make changes to the types of investments it uses.

Nine new investment default funds designed by employers and advisers were launched in 2019 and we are happy that the governance around these funds was robust.

2019 was a strong year for growth in investment markets following a disappointing 2018. At the time of writing our report this year, global markets are seeing significant falls as a result of the coronavirus outbreak. These falls have a direct impact on funds invested in equities (or company shares) and potentially other asset classes. Historically, following sharp falls such as these, markets do recover over time and it is important to remember that pensions are a long-term investment and that financial markets have always had ups and downs. We will report on the impact of current conditions on your investments and the ways in which the managers reacted in our report next year.

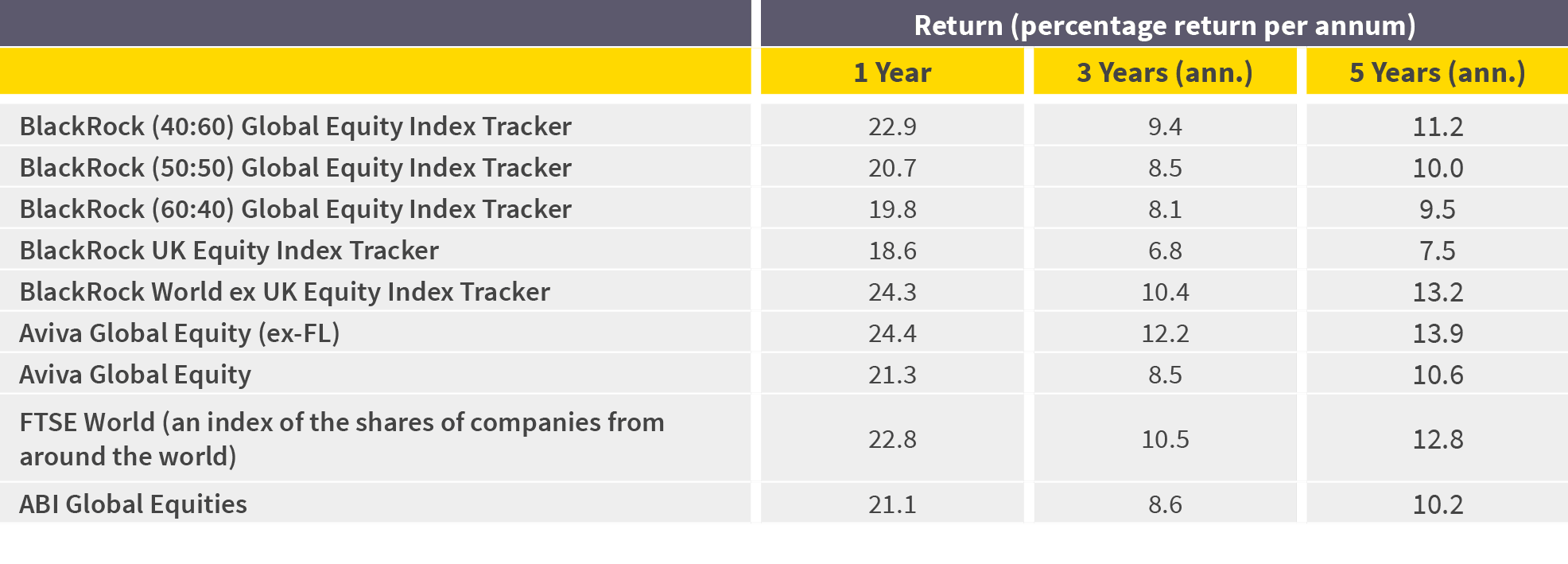

The performance of Aviva’s default funds for the year to December 2019, together with the performance of other multi-asset (those funds that invest in a range of different asset classes) and global equity funds are shown in the tables below together with comparative performance of industry sector “benchmarks” to provide an indication of how well Aviva’s funds have performed.

During the last year returns were, in all cases, considerably above interest rates on bank deposits and inflation, with the returns over three and five years strongly positive.

As always, please note past performance should not be seen as a guide to future returns.

Transaction costs are the costs of buying and selling shares and other assets which you incur when investing in funds. Fund managers are now required to disclose these costs to pension providers to enable there to be greater transparency around those costs incurred in managing each fund. The IGC is interested to see the absolute level of costs incurred within the funds in order to form a judgement on how reasonable they appear.

The method used by fund managers to calculate these costs is called “slippage cost”. This method calculates the difference between the expected price of trading a fund’s underlying investments, such as company shares or bonds, at the time the order is raised by the fund manager and the price at which the trade is executed on the relevant market. Calculating costs in this way can lead to a trading benefit to the fund as well as a loss (known as a negative cost).

Transaction costs are not deducted from your pension fund. They are reflected in the performance of the fund, so the higher the cost, the more it will impact on the fund’s annual return. The transaction costs for Aviva’s default funds and for the ten largest funds by assets under management are shown at Appendix B.

By their very nature, the transaction costs for actively managed funds will tend to be higher than for passively managed funds. These higher costs reflect the level of trading undertaken in the fund where managers look to take advantage of opportunities for growth, or to minimise losses.

As can be seen at Appendix A, the range of these costs for Aviva’s default funds is between -0.07% and 0.05% which the IGC feels to be reasonable. Now that transaction costs reporting has become more established within the industry, we will be benchmarking these costs against the default funds of other pension providers in next year’s report.

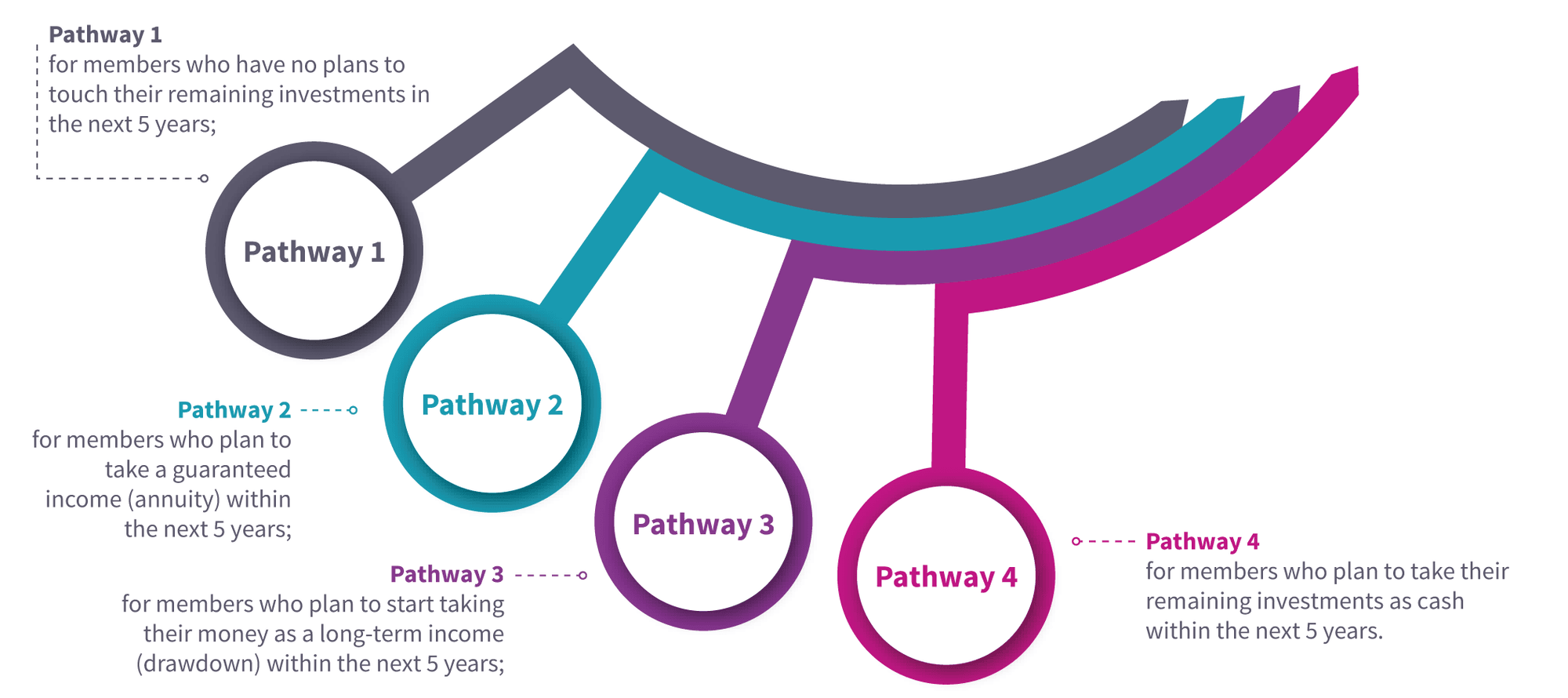

As mentioned earlier in our report, the FCA has extended the remit of IGCs to report on the value for money provided by what are referred to as investment pathway solutions. Aviva has seen a significant change in behaviour by customers since the introduction of pension freedoms and the option to take pension funds when they are needed rather than take an annuity. They are seeing increasing numbers of people take their tax-free cash but leave the rest of their money invested.

The FCA were concerned that these investments were being left in cash which could remain the case for several years to come before customers decided what to do with their money. Information provided to us by Aviva suggest that in reality members of workplace pension schemes do not put their pension savings in cash and only around 3% of customers take their tax-free cash and hold 50% or more of their remaining investments in cash.

Investment pathways are designed to provide a solution, and providers are now required to provide pathways which cater for each of the following scenarios

The IGC has been working with Aviva’s investment team to understand more about their proposed solution which is being finalised. We will be looking to ensure that whatever they implement is a suitable solution and that it represents value for money. We will also be looking at the communications which are provided to members to ensure they are clear and fit for purpose.

Pathways will be introduced later this year and we will report on the outcome in our next report.