In February 2021, Aviva launched a series of funds aligned to these Pathways. These are designed to provide customers with a choice of where to put their money when they take their retirement benefits and are broadly based around the pension options open to them. The FCA now require IGCs to undertake a Value for Money assessment of these new funds.

This report only covers the period to 31st December 2020, and so we will not be reporting on the launch itself, nor how many customers have chosen each of the four Pathway Funds until next year.

We spent a significant amount of time, as required, assessing the design of the Pathways from a Value for Money perspective. This covered investment make-up, costs and charges and the communications issued to members to explain their options. Separately, if your employer is advised by Mercer you are likely to be invested in a Mercer Workplace Savings product, and so we were also required to undertake the same assessment for Mercer’s Investment Pathways.

The aims of the four Pathways are broadly aligned to options available when people reach retirement. These options are common to all providers of Pathways and are not unique to Aviva, and so the Mercer Pathways also reflect these aims, albeit that the mix of assets may differ between Aviva and Mercer:

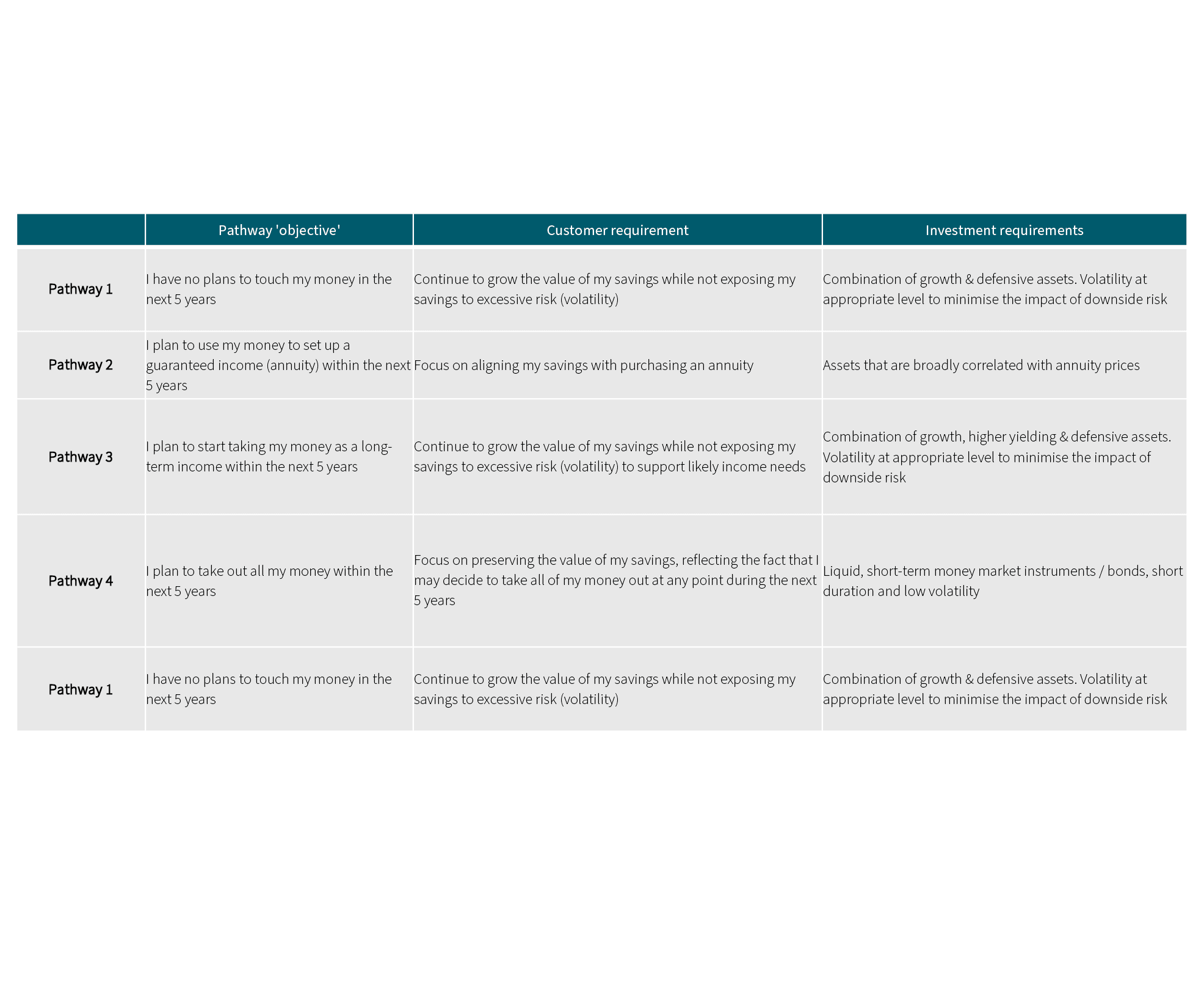

Pathway 1: I have no plans to touch my money in the next 5 years (Do nothing). It aims to provide an appropriate balance between growth and risk through exposure to a range of asset classes, that can include, but is not limited to, equities, fixed interest, cash and property.

Pathway 2: I plan to use my money to set up a guaranteed income within the next 5 years (Annuity). The fund will predominantly invest in UK Government and Corporate bonds.

Pathway 3: I plan to start taking my money as a long-term income within the next 5 years (Drawdown). It aims to provide an appropriate balance between growth and risk through an exposure to a range of asset classes that include, but is not limited to, equities, fixed interest, cash and property.

Pathway 4: I plan to take out all my money within the next 5 years (Cash). It seeks to achieve a positive return (before charges) by investing primarily in fixed interest and money market instruments.

To meet the stated aims and objectives, Aviva and Mercer have designed Pathway solutions which uses their own underlying investment funds. These are broadly similar in their construction. The rationale for the investment solution and design was based on both the objective of the Pathway and the customer requirement. These were as follows:

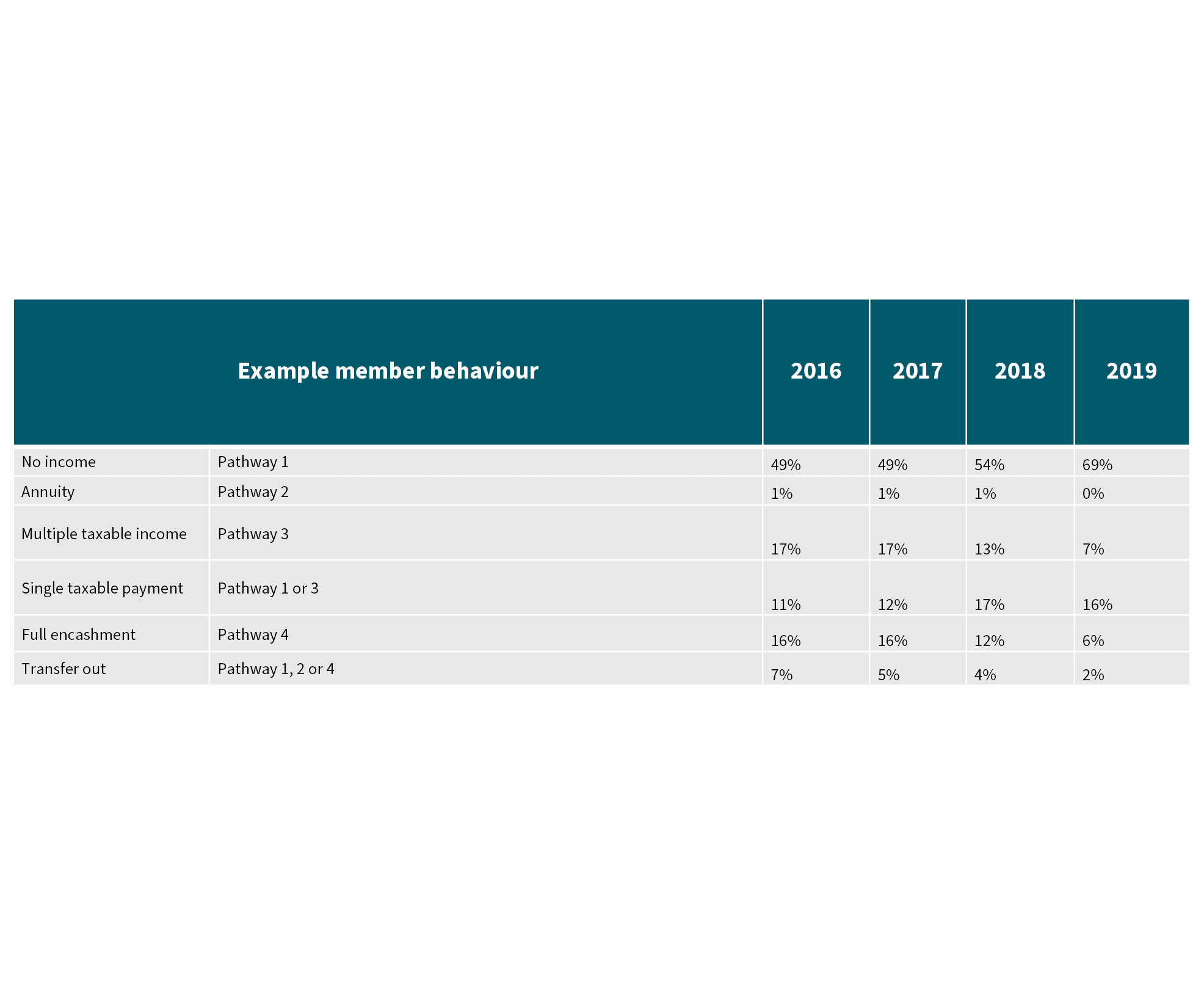

Aviva carried out some analysis of how members had been taking their benefits over the last few years in terms of type of options chosen, age that they took benefits and so on. They built the Pathways taking account of the different views that members might have towards risk and their desire to seek good investment returns. They carried out modelling around the possible outcomes that members might receive, and the level of risk involved with each Pathway to check that they were appropriate.

Analysis of member behaviours since 2016

Aviva also sought external independent views on the appropriateness of the Pathways from a firm specialising in combining actuarial knowledge, asset modelling and risk management. They concluded that each of the Pathways was appropriate and efficiently reflected the aims and objectives of each Pathway. The IGC received all reports and discussed these with the external firm and agreed with the conclusions. We will continue to assess the suitability of the Pathway design as we learn more about member behaviours.

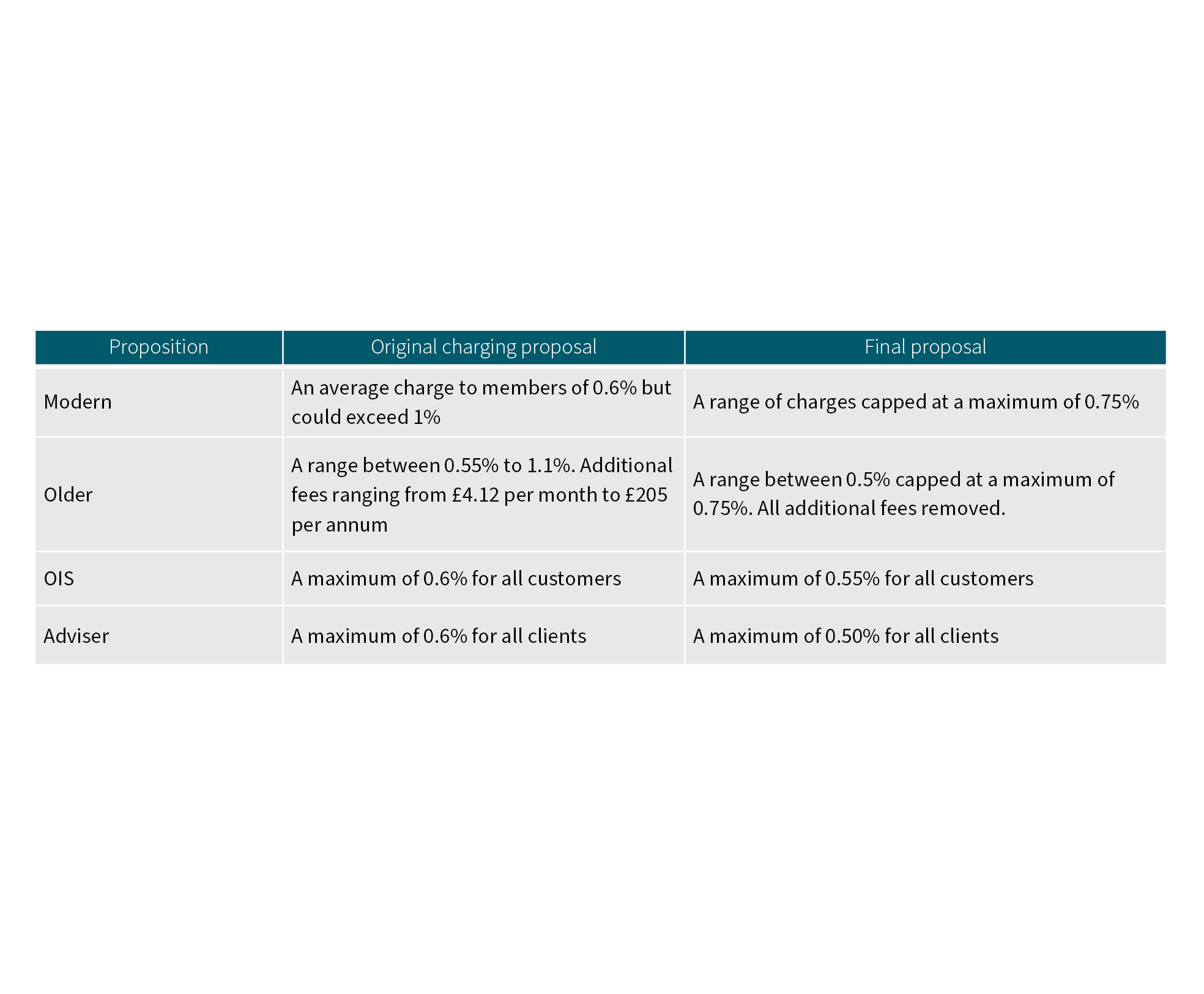

When Aviva first shared their proposals for Pathways with us, they explained that the costs and charges structure was broadly split into four different propositions:

The OIS and Adviser platforms do not offer workplace pensions, but as they offer Investment Pathways, we need to include them in our assessment.

Charges are set at different levels for each of these areas for Investment Pathways due to the nature of the proposition and the cost of operating the platform and the investments.

When we were first presented with the proposed charging structures, we challenged Aviva to reduce these in areas where we felt they had not accounted for the suggestion by the FCA that firms should use the 0.75% per annum charge cap as a guide to what value for money might look like. Charges ranged from a low level up to 1.1% per annum, but for some products also included a monthly or fixed charge for members entering drawdown.

We are happy that Aviva took on board our challenge and made significant improvements to the charging structures. We view these positively, particularly as members in modern products, which represent the majority of members, will never pay more in a Pathway than they are paying in their workplace pension.

At the time these charging levels were agreed, there was little or no evidence of how they compared with competitors. Now that Pathways have been launched, we will let you know how they compare with charges being made by other providers in our report next year.

Aviva has issued new communication material, or updated existing documents, to ensure members are aware of Investment Pathways, what their aims and objectives are and what they can do if they wish to enter a Pathway. We reviewed a number of documents and communication materials and made suggested changes to Aviva which they have adopted.

We found the documents to be clearly written and illustrated. The website Aviva has designed for the OIS and Adviser platforms is simple to navigate with clear instructions and the appropriate risk warnings are in place.

At relevant points in the journey, Aviva remind members that they do not have to remain in the same Pathway. If their circumstances change, they are able to switch to a more appropriate Pathway. There are reminders that financial advice should be taken for key decisions, and we are happy with the telephone triage service they have implemented which clearly explains options, risks and the investments designs themselves. We are happy to say that Aviva’s Investment Pathways communications are fit for purpose and that they take your interests into account in their design.

We have assessed Aviva’s Investment Pathways and feel that, based on what we know so far, they offer Value for Money and that the designs are appropriate for the objectives of each Pathway solution. We will make a more thorough assessment next year when we have evidence of how the costs and charges compare with other providers . There has been a significant change to member behaviour over the past few years. We will continue to monitor member behaviour patterns around the choice of Pathways and the extent to which members change their decisions. We will seek feedback and management information from Aviva so that we can look to ensure that the investment design of the Pathways remains appropriate.