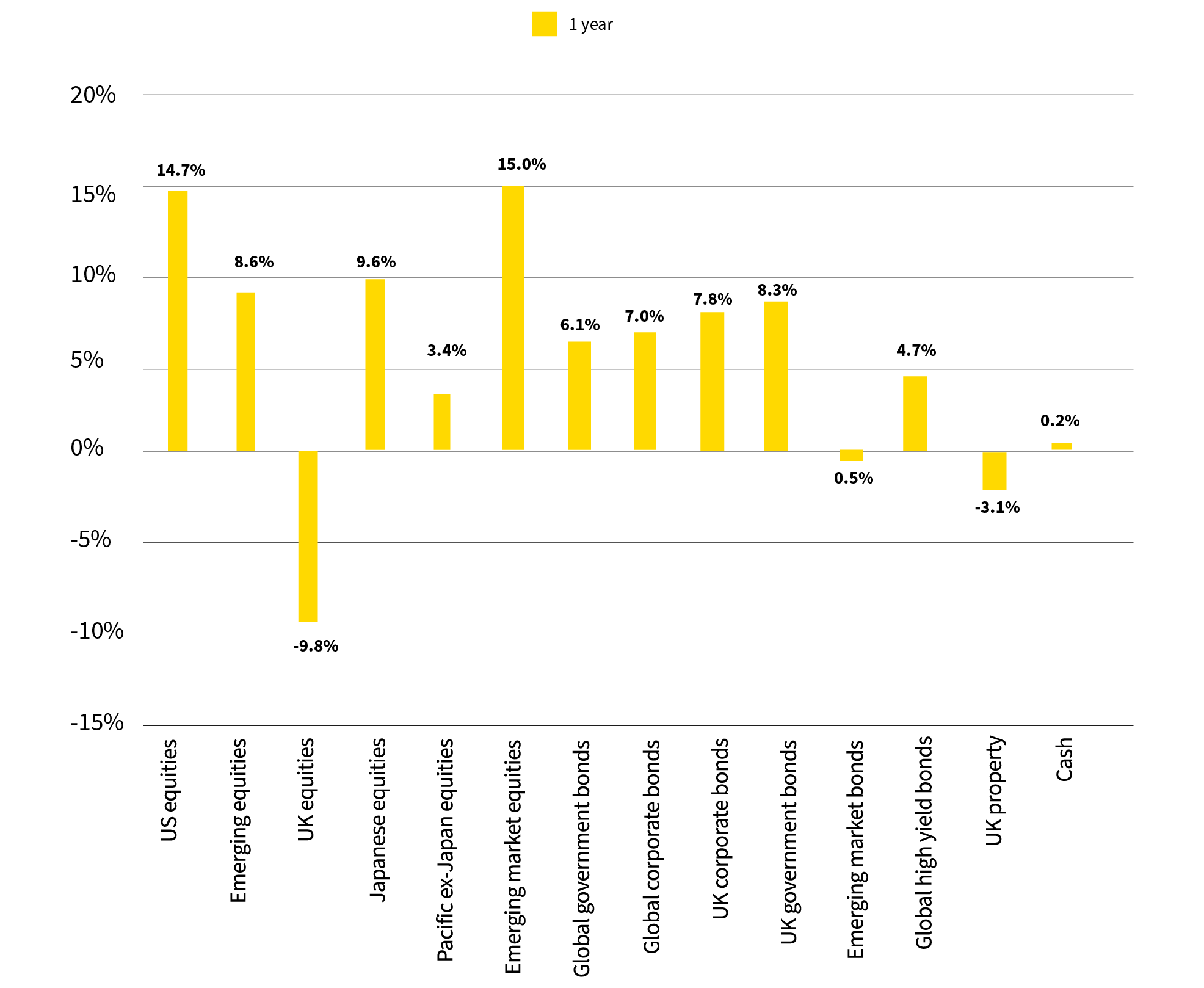

2020 was a turbulent year for global stock markets. We saw big falls in equities during the early months of the year at the start of the pandemic followed by a gradual recovery through the remainder of the year helped by the support provided to economies by Governments and Central Banks and latterly on positive news of vaccines against the virus. Some equity markets recovered better than others; upward progress was particularly strong in US equities and Emerging Markets equities but, coupled with the pandemic, the uncertainty around the ultimate Brexit deal caused UK equity markets to lag behind rises seen elsewhere.

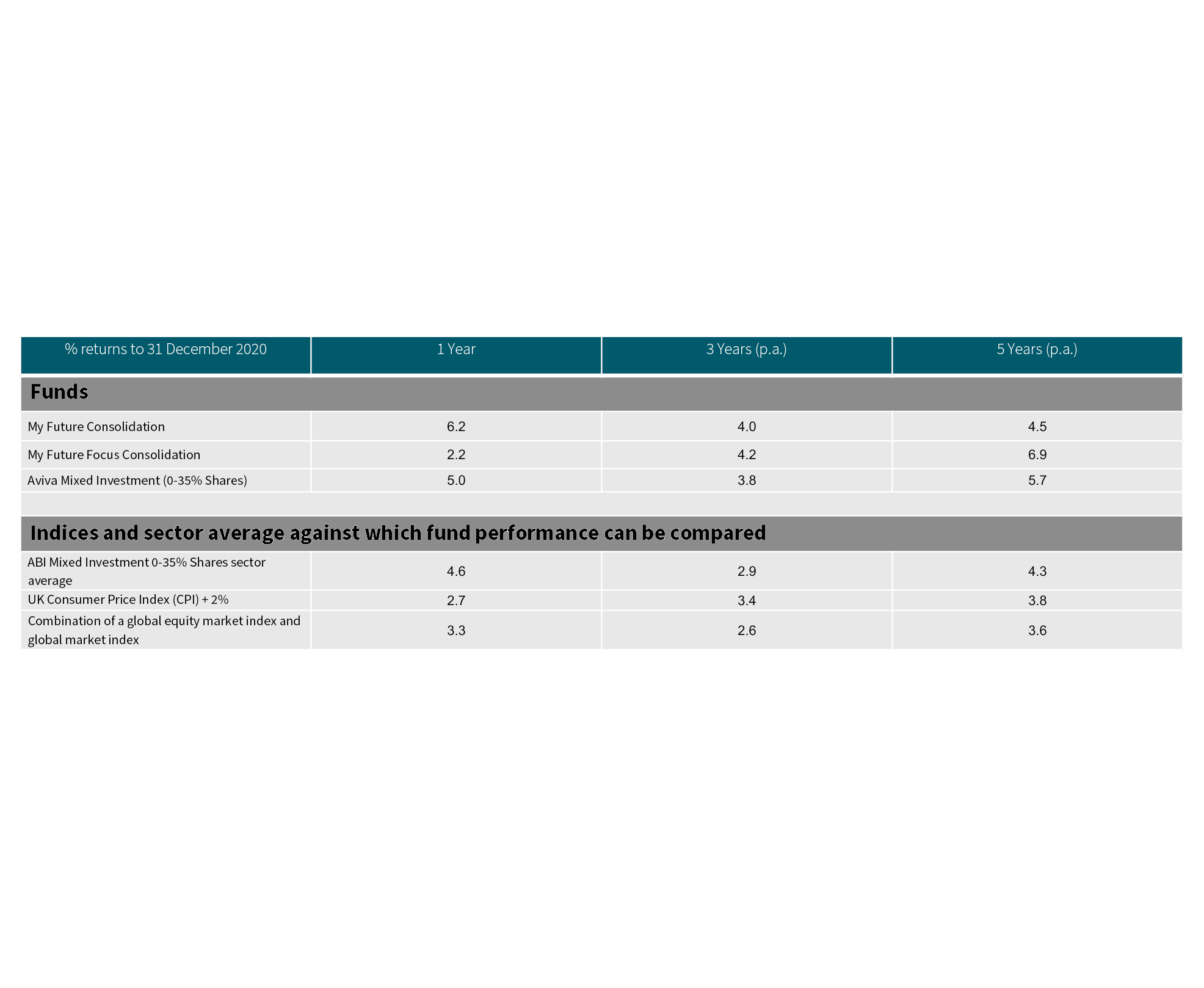

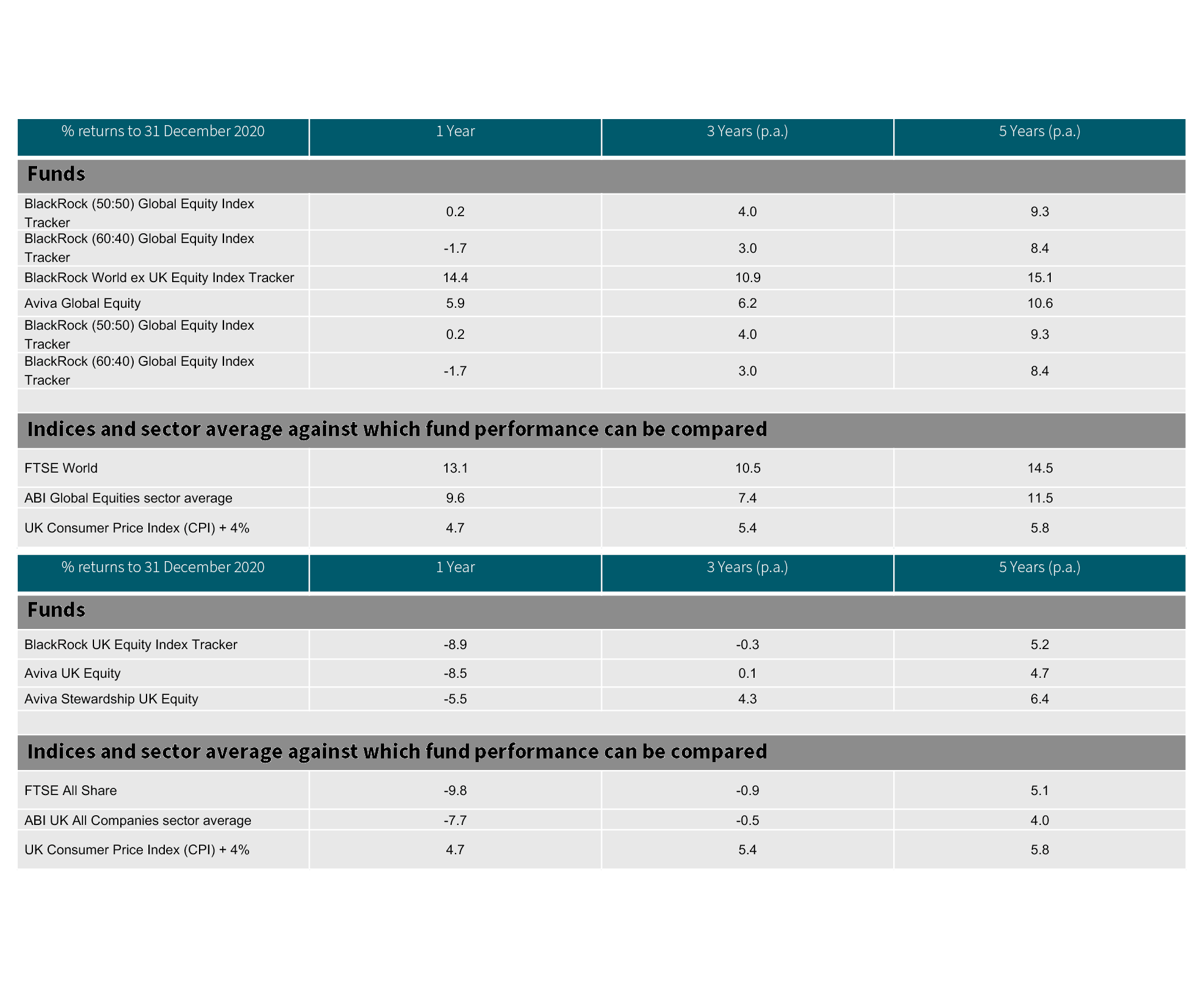

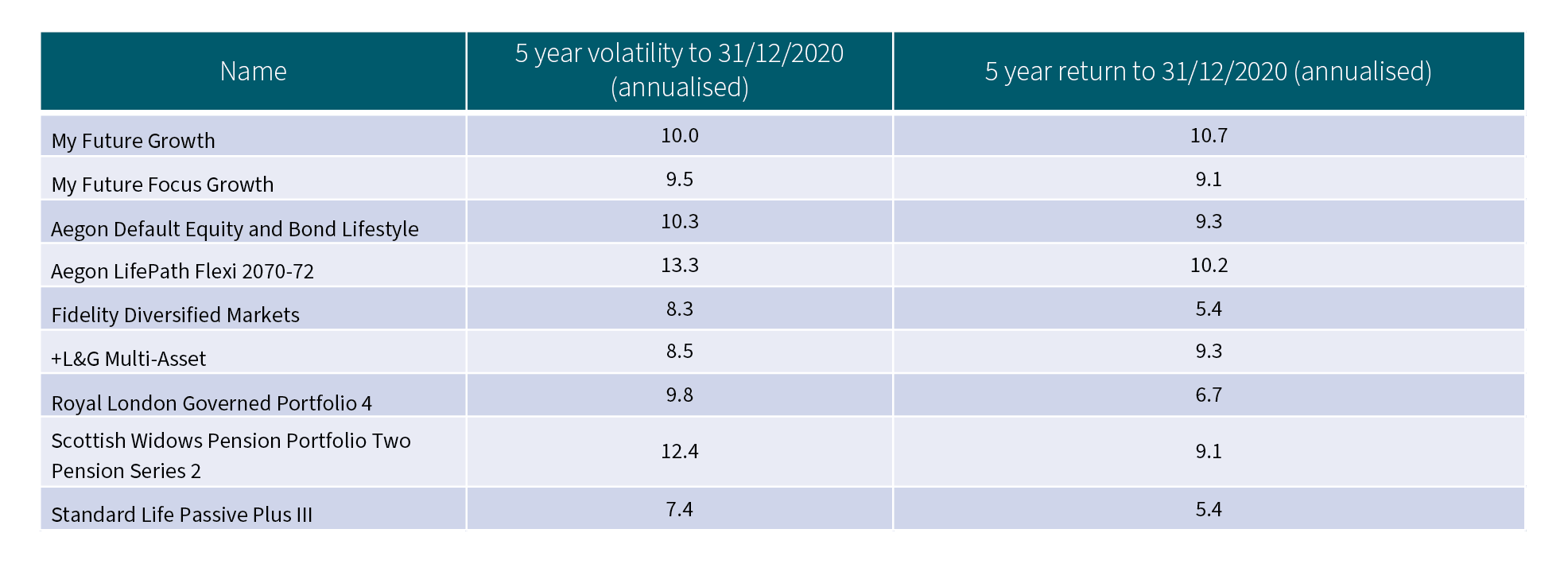

These tables show the performance of the top multi-asset funds (which include those used by the default investment funds for almost all members) and the top equity funds as measured by assets under management. This shows how global equity funds have outperformed UK equity funds. Investments with high exposure to UK equities have significantly under-performed when compared to those with no exposure. Most members in default funds, apart from those close to retirement age, are invested in the My Future Growth or My Future Focus Growth funds.

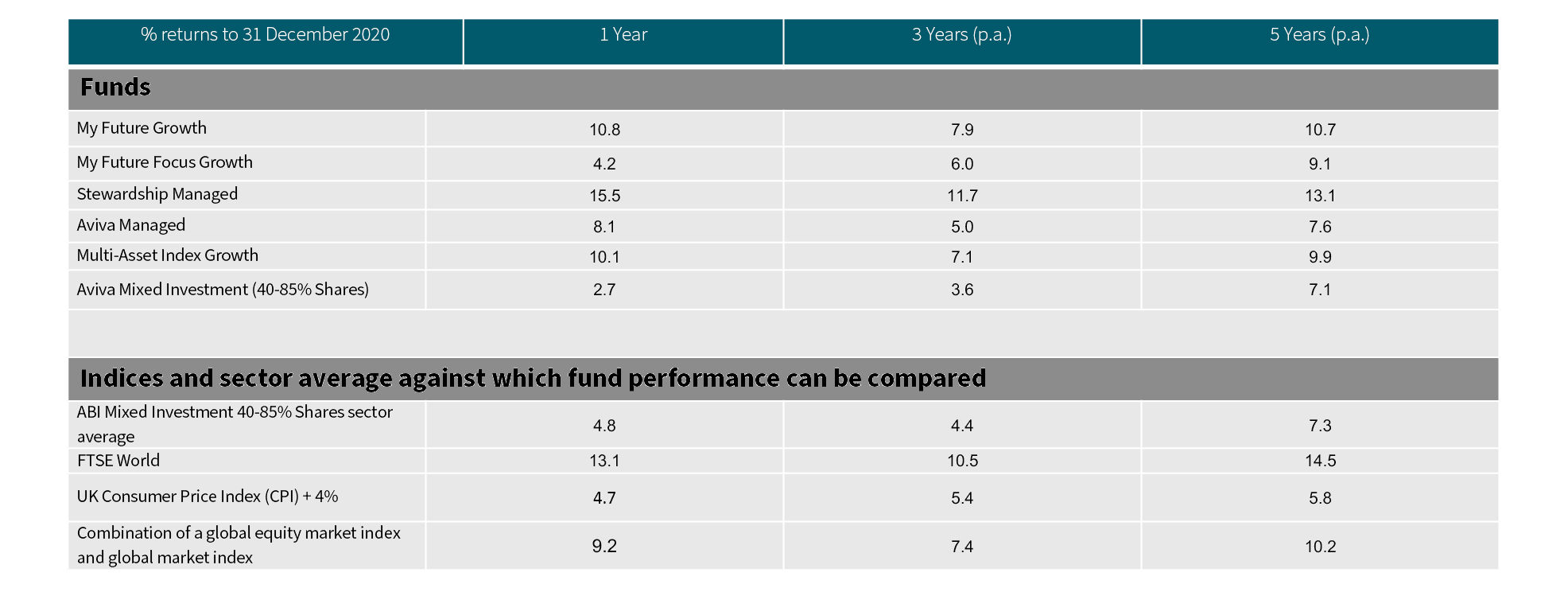

Source – Aviva

Despite the 2020 performance, we remain of the view that the wider diversity of assets within My Future Focus give the prospect of better risk-adjusted returns in the longer term. The fund also has a stronger emphasis upon Environmental, Social and Governance (ESG) considerations within the investment process and Aviva is seeing many employers and advisers placing a higher degree of importance to ESG factors. You can read more about this in the ESG section of this report.

These tables also show the importance of taking a long-term view of investments. The five-year performance figures show the average year-on-year returns achieved by the multi-asset funds which have delivered good above inflation returns to members. This is considered as a key performance indicator for the IGC alongside comparisons with similar funds in the market when evaluating the performance. It is important to note that past performance should not be used as a guide to future returns.

Source - Aviva

Unless you make an active choice of an alternative fund, you will be invested in your employer’s default investment fund. Over a million of you invest in Aviva’s two core default funds – My Future and My Future Focus.

My Future invests in passively managed funds with BlackRock Investment Management Limited being responsible for deciding the allocation between the different types of investments within the funds.

My Future Focus invests in both passively and actively managed funds but with Aviva Investors Multi-Asset investment team being responsible for deciding the allocation between the different types of investments.

In both cases, the allocations to the different types of investments will vary over time depending upon the investment managers’ views on expected future risk and returns.

My Future has a 15-year glidepath, and so if you invest in this fund, Aviva will automatically start to “de-risk” your investments when you are 15 years from retirement. For My Future Focus, the glidepath is 10 years.

The difference between the two glidepaths arises from the managers’ different views on the expected volatility and returns from the various asset classes. Before you reach your glidepath, you are invested in the “growth” element of the fund which aims to maximise the return on investments whilst minimising the level of investment risk (or volatility) to which your investments are exposed. The assets within the growth fund as at the end of 2020 is shown in the charts:

The IGC employed the services of a leading independent investment consultant to review Aviva’s default funds this year. We have recently received their report and will consider the detailed findings as part of our business plan for 2021/22. Some of the key headlines from their report are summarised here:

The default fund is appropriate and suitable for its members in terms of its core objectives

Assessed against a number of criteria used by the investment consultant, the default fund is classed as either “fit for purpose” or “best in class”

It has performed well relative to its competitors being 3rd out of 13 providers for the growth phase and 8th out of 13 for the “At retirement” phase over the 3-year period to 31 December 2020.

The growth and “At Retirement” phase could consider more diversification in asset classes which may improve members outcomes. However, one of the challenges for Aviva is that My Future is a low-cost solution and introducing other asset classes might increase charges.

The 15 year de-risking glidepath should be reviewed to see if member outcomes could be improved by shortening the glidepath or altering the level of investment risk with the growth phase.

We have included all the above areas in our business plan for discussion with Aviva over 2021/22. The consultant’s comments on ESG within the fund are noted in the ESG section of this report.

This default fund remains appropriate and suitable as a default strategy

Assessed against various criteria used by the investment consultant, the default fund is classed as either “Fit for purpose” or “Best in Class”. Importantly, ESG integration was cited as “Best in Class” which is in line with the IGC views on ESG.

This past year, whilst the fund was very diversified, its performance has been at the lower end compared to some of its peers in the market. This is because it holds less in equities compared to peers and equities performed very well over 2020.

The asset allocation at retirement may be out of line with the market in terms of the allocation to cash and lower equity allocation. We will be discussing these points with Aviva.

The 10-year glidepath is deemed to be appropriate taking account of the fund’s risk and volatility objectives.

Aviva operate a robust investment governance process to assess all funds, both internal and external, to ensure that their aims and objectives are being met. Should they not be, they will be placed on a watch list and the fund manager will be asked to address any failings. Should these failings not be addressed, they are removed from Aviva’s investment range. The IGC has attended Investment Governance Committee meetings to gain first-hand experience of how they operate, the processes followed, and the robustness of the decisions reached and will continue to attend future meetings periodically.

In 2020, a review of the range of funds available across Aviva was completed which had been underway for four years. The aim of this review was to identify those funds which had not accumulated significant assets since launch and so were sub-scale. Where possible, those funds with less than £10m of assets were reviewed and closed, although this was not done on a blanket basis, with some being retained if it was felt they still had a particular part to play in the choice for members or if they were new funds. The review led to the closure of over 300 funds from a cost, governance and/or risk perspective.

The standard governance process was run alongside this activity. Members within the funds being closed were transferred to an appropriate equivalent fund if they had not made an alternative selection themselves. This has been a significant undertaking by Aviva and clearly demonstrates that their investment governance encompasses all investments and not just the default investment funds.

During 2020, Aviva launched 21 new funds, including 7 new employer or adviser designed funds. All these new funds were put through the investment governance process and 4 funds not felt to be suitable were rejected. For new default funds, Aviva will not accept any new default arrangements which specifically target an annuity.

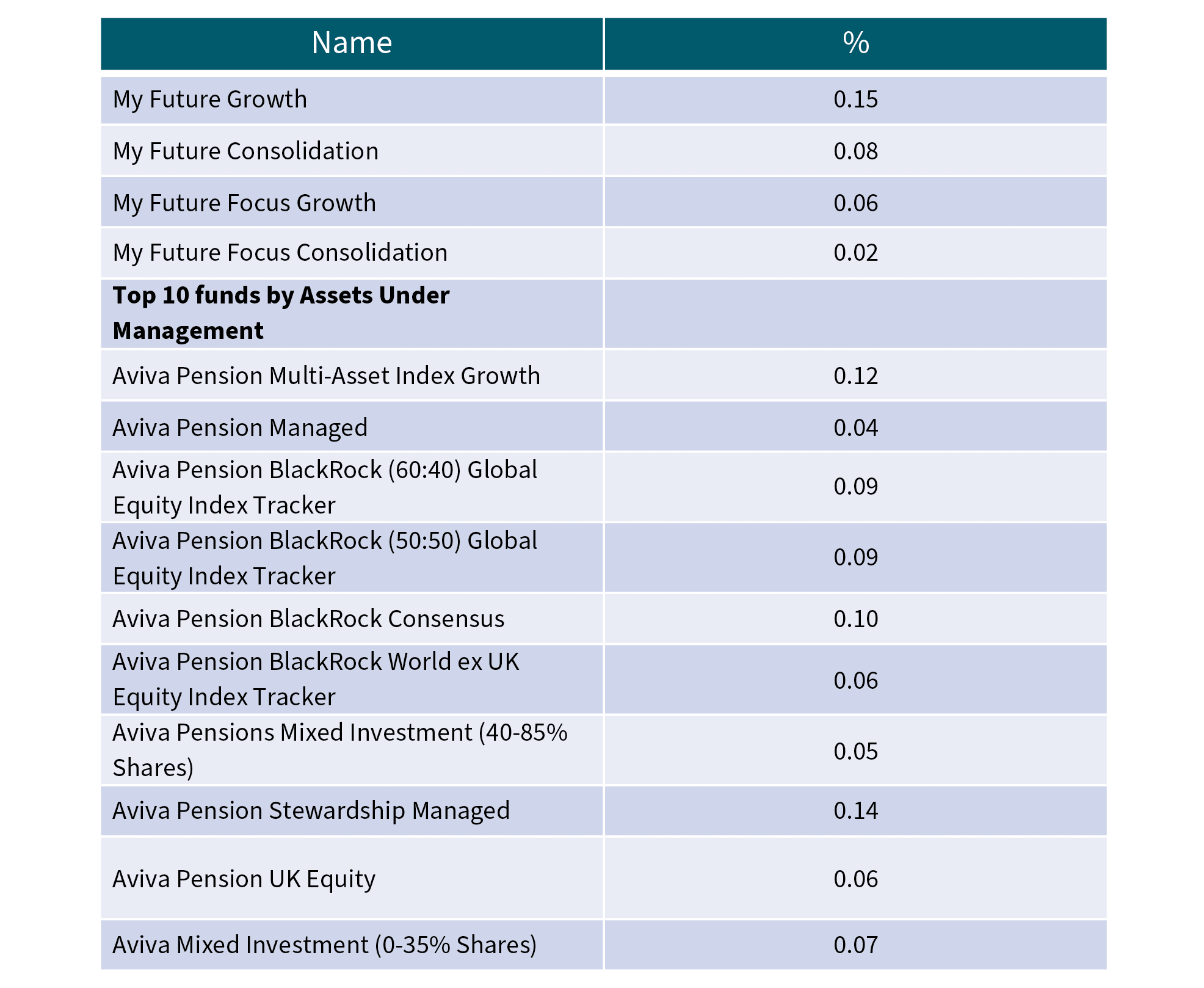

Transaction costs are not included in the charge cap of 0.75%. It is also not a charge that you pay directly, but rather has an impact on the investment returns you receive from your chosen investment.

Aviva provided us with details of transaction costs for all of the investments available to you. These showed a significant variance in transaction costs with a range varying from a negative cost to a charge of over 2%. The costs for Aviva’s own default funds were at the much lower end of the scale as can be seen in the table:

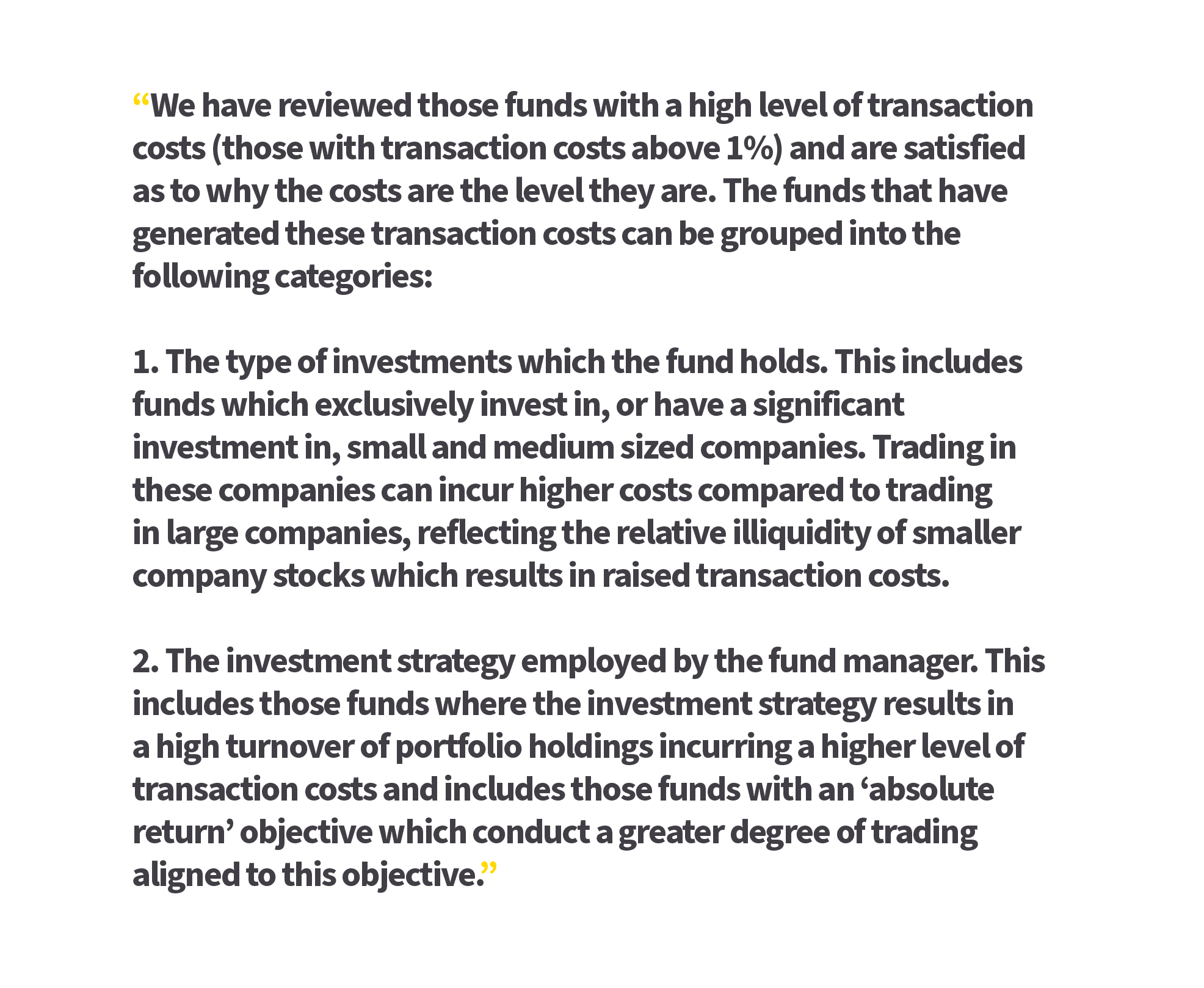

We asked Aviva to explain why some funds were showing such high transaction costs when compared to others. They responded with the following:

We are satisfied that Aviva has a robust investment governance process in place and that this identifies those funds which do not perform as expected or are not a popular investment choice. Performance of their own default funds has been strong in relation to other providers (taking account of the level of risk/volatility associated with each fund) and has held up well against the backdrop of challenging investment conditions.

Independent advice supports the IGC’s own view that both the My Future and My Future Focus default funds are appropriate and suitable for its members, but there are some areas where enhancements could be made – we will be discussing these with Aviva during 2021/22.

While transaction costs were high for a small number of funds we are satisfied with the overall explanations for Aviva controlled funds. Other funds will be reviewed by the Aviva investment governance process including taking any higher than expected transaction costs into consideration.

Aviva’s own default investment funds provide a low-cost solution for members.