Statement of Investment Principles

The Scheme is designed for multiple employers, but delivered under a single trust arrangement and governed by a Board of Trustees, chaired by Elizabeth Renshaw-Ames. A specialist independent investment adviser (Isio), legal advisers (Squire Patton Boggs and Sackers) and auditor (RSM) make up the team of experts that supports the Trustees to deliver strong governance standards.

This Statement of Investment Principles (“the Statement”) states the investment principles governing decisions about investments for the purposes of the Scheme, a defined contribution pension arrangement made up of a number of employer-specific arrangements, registered with HMRC under Finance Act 2004. It has been produced by the Trustees of the Scheme in compliance with section 35 of the Pensions Act 1995 and any relevant subsequent legislation.

The Statement, which has been prepared by the Trustees of the Scheme, will be made available to all participating employers prior to selecting the Scheme. All advice the Trustees receive regarding investment options for an employer of the Scheme will make reference to the Statement and indicate how the principles defined within it have been addressed. It will also consider the appropriateness of fees and charges payable by members of the Scheme.

The Scheme invests by way of investment policies with Aviva in pooled funds accessed via the Aviva investment platform. It offers a large, diverse range of pooled funds from which investments can be selected in each section on the Scheme. In agreeing to this arrangement, the Trustees have specified that the Scheme’s fund range should:

The day-to-day management of the Scheme’s assets is ultimately delegated to one or more investment managers via insurance contracts or investment management agreements.

The Scheme offers a standard section that falls solely under the governance remit of the Trustees. In addition, employers are able to take independent advice and should they wish, establish their own bespoke default investment option or other investment options. The Trustees remain fully responsible for the governance of all these investment options.

Details of the default investment options for the standard section of the Scheme are contained in Appendix 1.

Where an employer requests that the Trustees establish a bespoke default investment option and/or fund range, details are contained in a separate “Employer Specific” document which can be found in Appendix 2.

For all sections of the Scheme, the Trustees will consider how best to safeguard members from the risks associated with investing their pension savings. The following list summarises some of the key risks and how the fund range is designed in light of these:

Inflation – Taking the fund range as a whole it is expected that the performance of member funds should protect the real value of their pension savings over an appropriate time horizon.

Shortfall – Although the Trustees have no influence over the level of contributions paid, members may potentially receive a lower retirement benefit than they had hoped for. The Trustees will inform members annually of the projected value of their pension account at retirement in order to inform their decision making.

Performance ups and downs – Those funds which have a chance of achieving higher returns for members are likely to see greater volatility over shorter time periods. An appropriate level of risk for a specific default investment option will be considered against the profile of the membership.

Pension conversion – For members approaching retirement, the impact of poor performance is significantly increased as they have less time to make up any lost money. Default investment options may factor in a de-risking mechanism such as lifestyling that recognises the changing requirements of members as they approach retirement, for example with a greater focus on capital preservation.

Manager – There is no guarantee that any fund within the default investment option or self-select range will achieve its long-term objective. The Trustees will continue to monitor the funds and managers available to Scheme members to try and minimise this risk as much as is practically possible.

Diversification – Failure to diversify increases the risk of losing money if one particular investment does not perform as expected. A default investment option will need to contain an appropriate level of diversification.

Liquidity – Some investments types are not easy to sell (for example, real estate), potentially resulting in a delay in buying or selling assets. The use of investments that may have liquidity issues will be restricted unless this risk is specifically managed.

Credit – The risk that one party to a financial instrument will cause a financial loss for the other party by failing to discharge an obligation, either directly or indirectly. The Scheme is subject to credit risk through its investment policy with Aviva, and through the underlying investments in the underlying funds. Aviva is regulated by the Prudential Regulation Authority and the Financial Conduct Authority and, in the event of default by Aviva, the Scheme is protected by the Financial Services Compensation Scheme. The Trustees monitor the financial strength of Aviva and the security of the Scheme assets in conjunction with their specialist independent investment adviser.

Market – The Scheme is subject to a number of market risks:

Environmental, Social and Governance Factors – Management of investments with regard to Environmental, Social and Governance (ESG) factors, including but not limited to climate change, can impact performance and member outcomes. The Trustees have formulated their own set of ESG beliefs as detailed in the Trustees’ ‘Environmental, Social and Governance Policy Statement’ which is set out in Appendix 3. The Trustees have carried out a detailed process to formulate their beliefs and to reflect the importance they believe ESG factors should play in the Scheme’s investment strategy decisions. The Trustees’ ESG beliefs and Policy Statement will be reviewed on a regular basis.

The day-to-day management of the underlying investments is the responsibility of the underlying fund managers, including the direct management of credit and market risks. The Trustees monitor the Scheme’s investment options and the fund managers on a regular basis, with the help from its specialist independent investment adviser.

The overarching objective for the Scheme is to deliver long term positive returns, after charges, taking account of the risks described above.

The Trustees have regard to the relative investment return and risk that each asset class is expected to provide. The Trustees are advised by their independent professional advisers on these matters, who they deem to be appropriately qualified experts. However, the day-to-day selection of investments is delegated to the investment managers

The Scheme invests in pooled funds which can be quickly realised as required, under normal market conditions.

The Trustees have considered how financially material considerations, including ESG factors (which include climate change), are taken into account in the selection, retention, realisation and monitoring of the Scheme’s investment options over the appropriate time horizon applicable to members invested in those options.

As the Scheme invests via pooled funds, this means that the Trustees have delegated responsibility for the selection, retention and realisation of investments to the underlying fund managers of those funds (within certain guidelines and restrictions) and the Trustees’ approach to managing financially material considerations is limited by the nature of those pooled funds.

The Trustees also delegate exercise of the rights (including voting rights) attaching to the investments to the individual fund managers. Fund managers are expected to:

The Trustees have developed an Environmental, Social and Governance (ESG) Policy which has been integrated into monitoring the Scheme’s investment arrangements, this policy is provided in Appendix 3 and is reviewed by the Trustees on a regular basis. The Trustees believe that by including ESG factors in investment decision making, it will reduce overall investment risks whilst generating sustainable investment returns.

The Trustees do not take into account any non-financial matters (i.e. matters relating to the ethical and other views of members and beneficiaries, rather than considerations of financial risk and return) in setting the investment strategy for the default investment options for the standard section of the Scheme. However, the Trustees recognise the importance of offering a suitable range of investment options for members who wish to express an ethical preference in their pension savings. The Trustees may take non-financial factors into account in the self-select investment options for the standard section and in any bespoke default investment option or other investment options. The basis on which such factors are taken into account would be made clear in the description of such funds.

The Trustees engage with Aviva and the fund managers on the integration of ESG into the Scheme’s investments and how this can be improved.

The Trustees have adopted Aviva’s My Future Focus as the standard default investment option for the Scheme. The My Future Focus solution integrates ESG factors into its construction and ongoing management, with the use of ESG factors in stock selection and the application of an ESG focussed tilt on the passive regional equity investments, together with active voting and engagement.

In addition, the Scheme’s alternative default investment option (‘Aviva My Future') will be updated to incorporate the introduction of an ESG portfolio into the equity allocation of the strategy.

The Scheme also offers an additional ethical Lifestyle option and a range of funds incorporating both ESG and non-financial factors as part of the self-select fund range.

The Trustees continue to have aspirations to further develop the level of ESG integration incorporated within the default investment options and funds offered by the scheme.

The Trustees are working with Aviva to develop additional reporting, including specific ESG metrics, to measure the development of ESG within the overall investment arrangements.

The Scheme invests in pooled funds managed by one or more investment managers.

The Trustees select such funds with an expectation of a long-term appointment and ensuring that the investment objectives and guidelines of the fund are consistent with the Trustees’ investment policies.

The Scheme’s investments will be regularly monitored by the Trustees (with the assistance of its specialist independent investment adviser) over an appropriate time horizon, to consider the extent to which the investment strategy and decisions of the Scheme’s fund managers are aligned with the Trustees’ policies. This includes monitoring:

Fund managers are remunerated based on the value of assets which they manage for the Scheme and while there is no set duration for arrangements with fund managers, they can be replaced at any time by the Trustees. The duration of the existing manager relationships is summarised in Aviva’s quarterly reporting which they prepare for the Trustees. Where fund managers fail to adhere to the Scheme’s policies, the Trustees work with Aviva and engage with the manager to discuss how alignment may be improved. If, following engagement with the manager, it is the view of the Trustees that the degree of alignment remains unsatisfactory, the arrangements with the manager may be altered or their appointment terminated where this is deemed necessary.

The Statement will be reviewed triennially by the Trustees and without delay following any significant change in the Trustees’ investment policy.

In preparing the Statement, the Trustees have obtained and considered the written advice of a person who is reasonably believed by the Trustees to be qualified by their ability in and practical experience of financial matters and to have the appropriate knowledge and experience of the management of the investments of schemes such as the Scheme. The Trustees have consulted with Aviva Life and Pensions UK Limited (“Aviva”) as sponsoring employer and the company appointed to act on behalf of the participating employers to the Scheme.

Before revising the Statement at any time in the future, the Trustees will obtain and consider the written advice of a specialist independent investment adviser and will consult with Aviva.

Position: Chair of Trustees Name: Elizabeth Renshaw-Ames Date: 28 September 2020

The Trustees’ overall objective is to provide investment options that enable members to grow their pension savings after charges over the long term, and to manage risks appropriately.

The default investment options, as described below, are expected to meet this objective and also take into account guidance from the Pensions Regulator and the Department for Work & Pensions for offering a default investment option for defined contribution automatic enrolment pension schemes.

Furthermore, the Trustees believe that the self-select funds offered as an alternative to the default investment options enable members to choose their own portfolio of funds which would achieve the overall objective.

The Trustees have designated Aviva’s My Future Focus strategy as the standard default investment option for members, and this will be used as the default investment option by participating employers who do not request that the Trustees implement an alternative default investment option or bespoke default investment option.

This standard default investment option invests in the Aviva My Future Focus Growth Fund during the growth phase of the lifestyle strategy.

During the pre-retirement phase, starting 10 years away from retirement, members’ assets are phased such that the exposure to the Aviva My Future Focus Growth Fund is reduced and exposure to the Aviva My Future Focus Consolidation Fund is increased. At retirement a member will be 100% invested in the Aviva My Future Focus Consolidation Fund.

The Trustees have also designated Aviva’s My Future strategy as an alternative default investment option which employers may request that the Trustees invest in.

This alternative default investment option invests in the Aviva My Future Growth Fund during the growth phase of the lifestyle strategy.

During the pre-retirement phase, starting 15 years away from retirement, members’ assets are phased such that the exposure to the Aviva My Future Growth Fund is reduced and exposure to the Aviva My Future Consolidation Fund is increased. At retirement a member will be 100% invested in the Aviva My Future Consolidation Fund.

Where an employer requests that the Trustees establish a bespoke default investment option and/or fund range, details are contained in a separate “Employer Specific” document within Appendix 2.

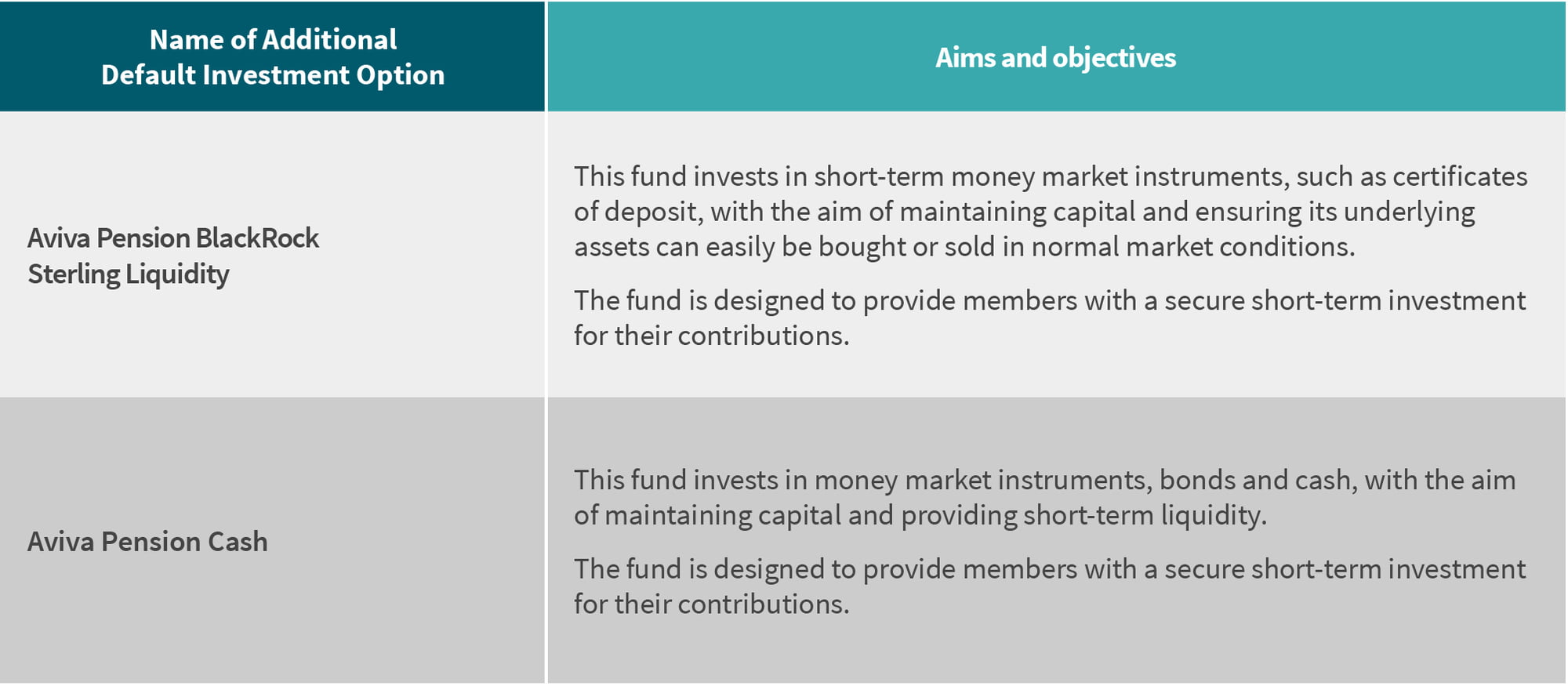

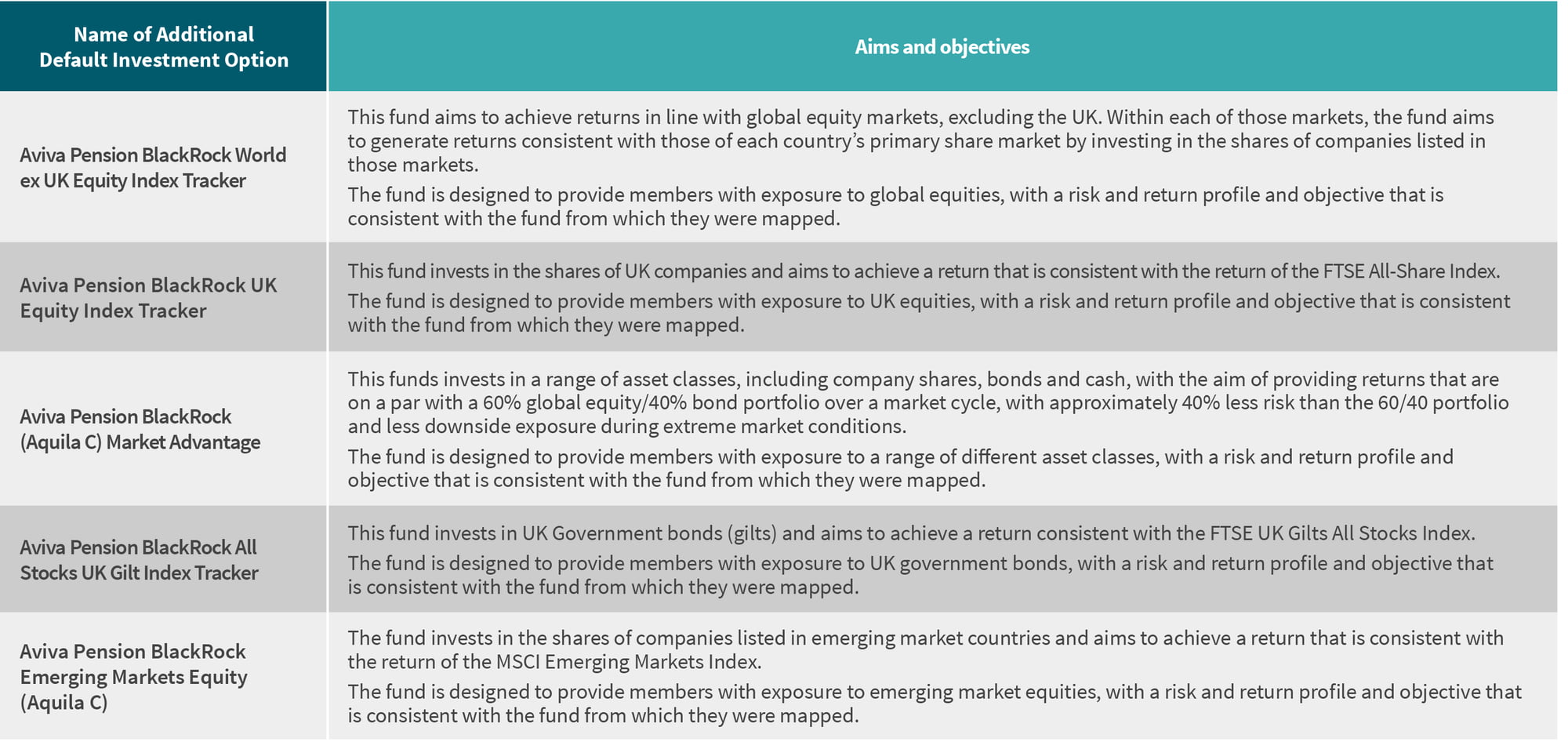

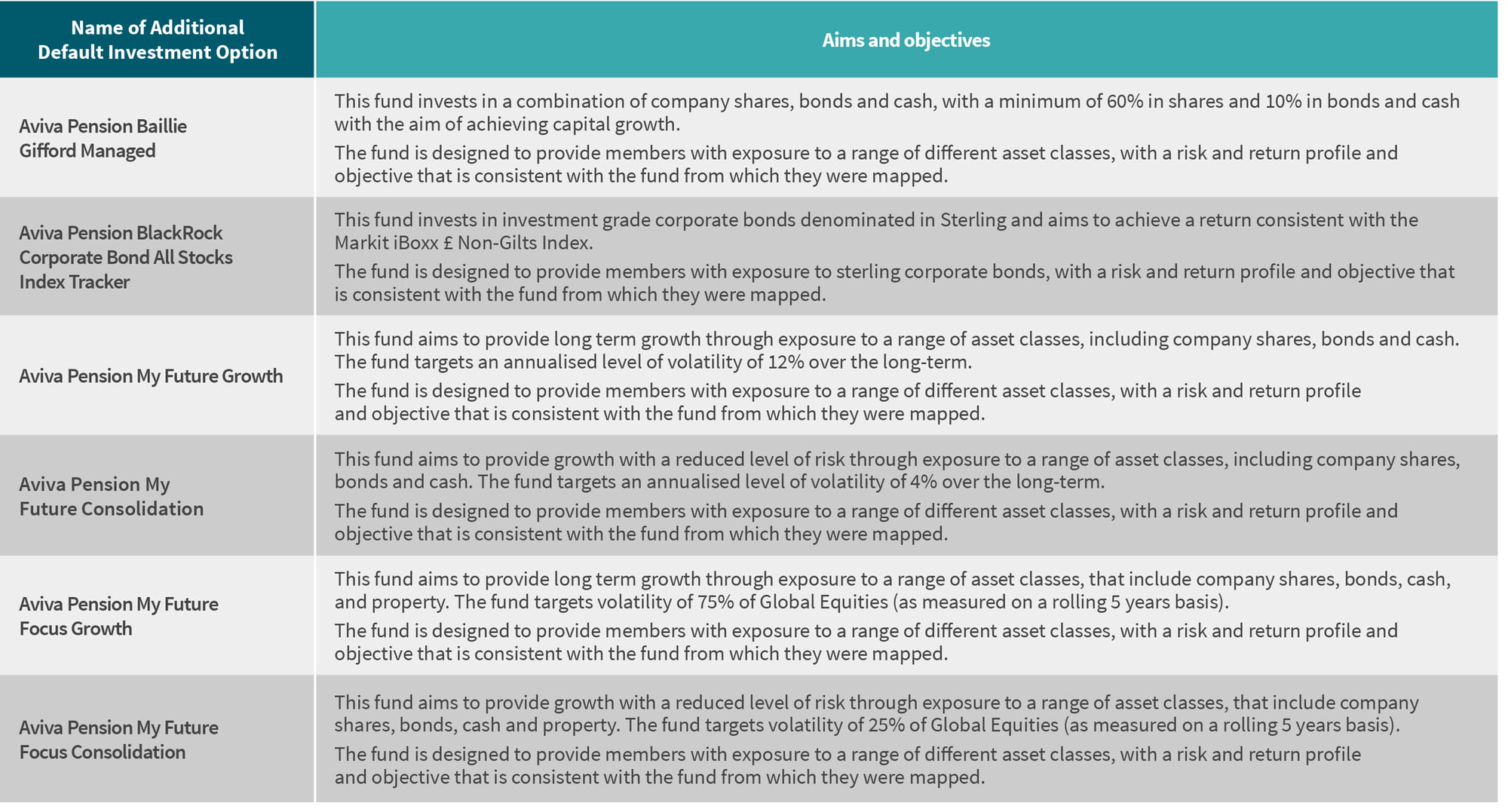

There are also a number of additional default investment options which have been made available to self-select members for two main reasons.

For some members who self-select their own funds, there has been a circumstance in which some cash funds have become a member’s default investment option. This has been triggered by two self-select Property funds being suspended to new monies and withdrawals.

The two default investment options that have resulted are shown below (together with aims and objectives):

The default investment options that have resulted are shown below (together with aims and objectives):

The Trustees’ wider investment policy and considerations as disclosed throughout this statement apply equally to the design and construction of the default investment options.

In designing the default investment options under the Scheme to ensure that assets are invested in the best interests of members, the Trustees, in conjunction with their investment advisers gave in-depth consideration to the demographic profile and expected member behaviour together with the retirement outcome needs and the risk tolerance of the membership. In addition, where relevant, consideration was given to the funds previously chosen by members and the similarity between the objectives of the Scheme’s fund options and those of the member’s most recent active fund choice. Due consideration was also given to compliance with the charge cap.

The Trustees will continue to obtain ongoing advice from its investment advisers relating to the ongoing suitability of the default investment options outlined in this Appendix as acceptable default investment options for the Scheme and that they comply with this statement of investment principles.

The retirement outcomes of the default investment options will be reviewed at least triennially or earlier in the event of any significant changes in the investment policy or member demographics. The review will take into account the manner in which members take their pension savings from the Scheme and any significant changes in the demographic profile of the relevant members.

Within the standard section of the Scheme the Trustees also offer a range of additional lifestyle options and self-select funds.

The lifestyle options available are targeted for different member outcomes: cash; drawdown; and annuity. It also includes an ethical lifestyle option, the Aviva Stewardship Lifetime strategy.

The self-select fund options encompass a wider range of asset classes including equity, fixed income and multi-asset funds, as well as the Stewardship range of funds which look to provide members with a range of funds with an ethical and ESG bias in their construction. Passive and Active options are available to members.

This Appendix is for the C&J Clark Section of the Aviva Master Trust. The Trustees have taken advice from Isio (formerly KPMG LLP’s UK pension practice) on the suitability of the investment strategy for this section.

The main investment objectives are:

A default option has been selected for the C&J Clark Section, and has been designed to be suitable for a typical member. The default has been chosen taking account of:

This default option invests in the Clarks Growth Fund during the growth phase of the lifestyle strategy.

During the transition phase, starting 20 years away from retirement, members’ assets are phased such that the exposure to the Clarks Growth Fund is reduced and exposure to the Clarks Retirement Transition Fund is increased. At the point 10 years from retirement a member will be 100% invested in the Clarks Retirement Transition Fund.

During the pre-retirement phase, starting 10 years away from retirement, members’ assets are phased such that the exposure to the Clarks Retirement Transition Fund is reduced and exposure to the Clarks Target Drawdown Fund and Clarks Cash Fund is increased. At retirement a member will be 40% invested in the Clarks Target Drawdown Fund and 60% invested in the Clarks Target Cash Fund.

The default option has been constructed so as to be suitable for members in light of the flexibilities available to members once they reach retirement.

The default investment lifestyle strategy will be reviewed at least triennially or earlier in the event of any significant changes in the investment policy or member demographics. The review will take into account the manner in which members take their pension savings from the Section and any significant changes in the demographic profile of the relevant members.

In addition to the default the members can choose from the full range of self-select fund options offered through the standard section of the Scheme, as well as a number of additional funds.

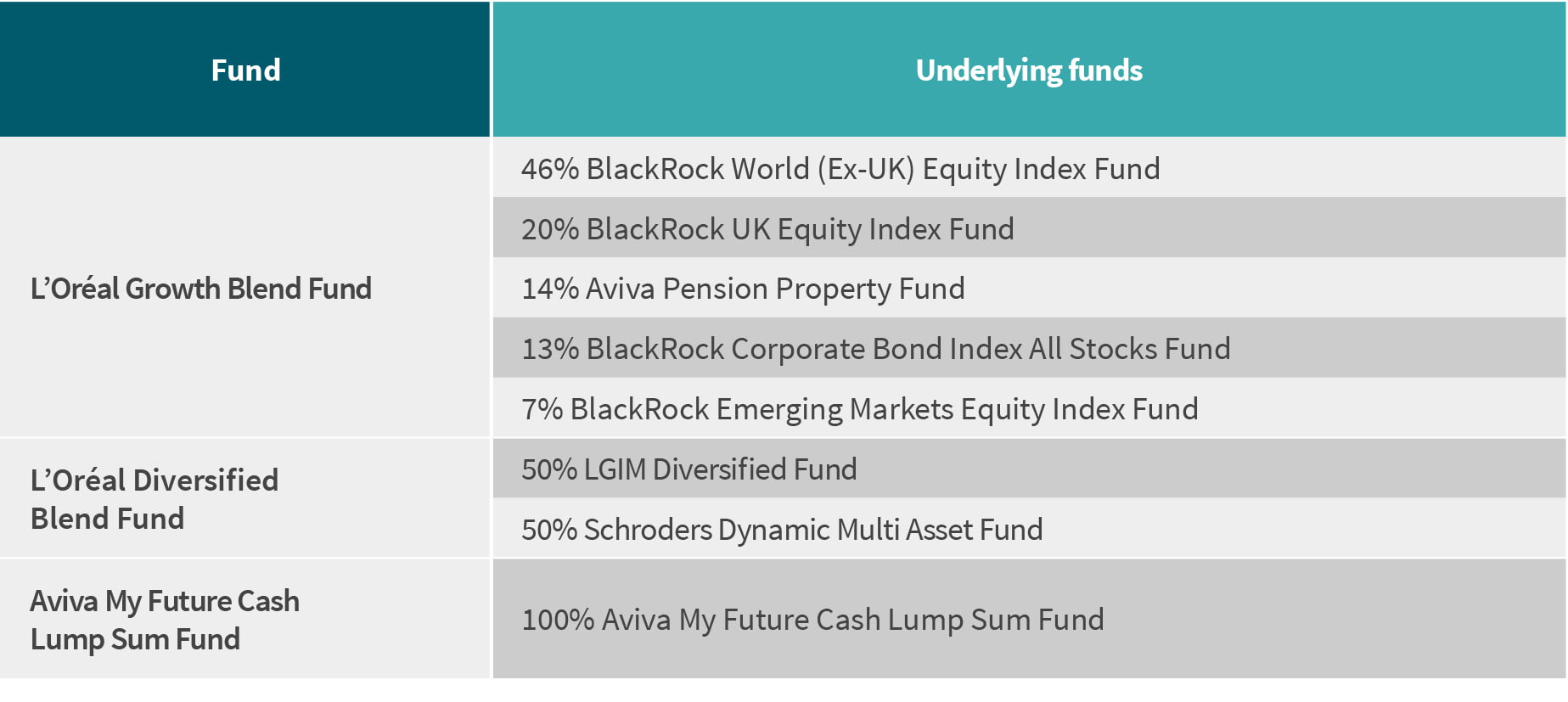

This Appendix is for the L’Oréal Section of the Aviva Master Trust. The Trustees have taken advice from Hymans Robertson LLP on the suitability of the investment strategy for this section.

A default option has been selected for the L’Oréal Section, and has been designed to be suitable for a typical member. The default has been chosen taking account of:

Based on analysis on the projected pot size for members less than 10 years to retirement and recent experience of how members in the Plan have been taking their retirement benefits, it is expected that members will take a one-off cash lump sum or UFPLS.

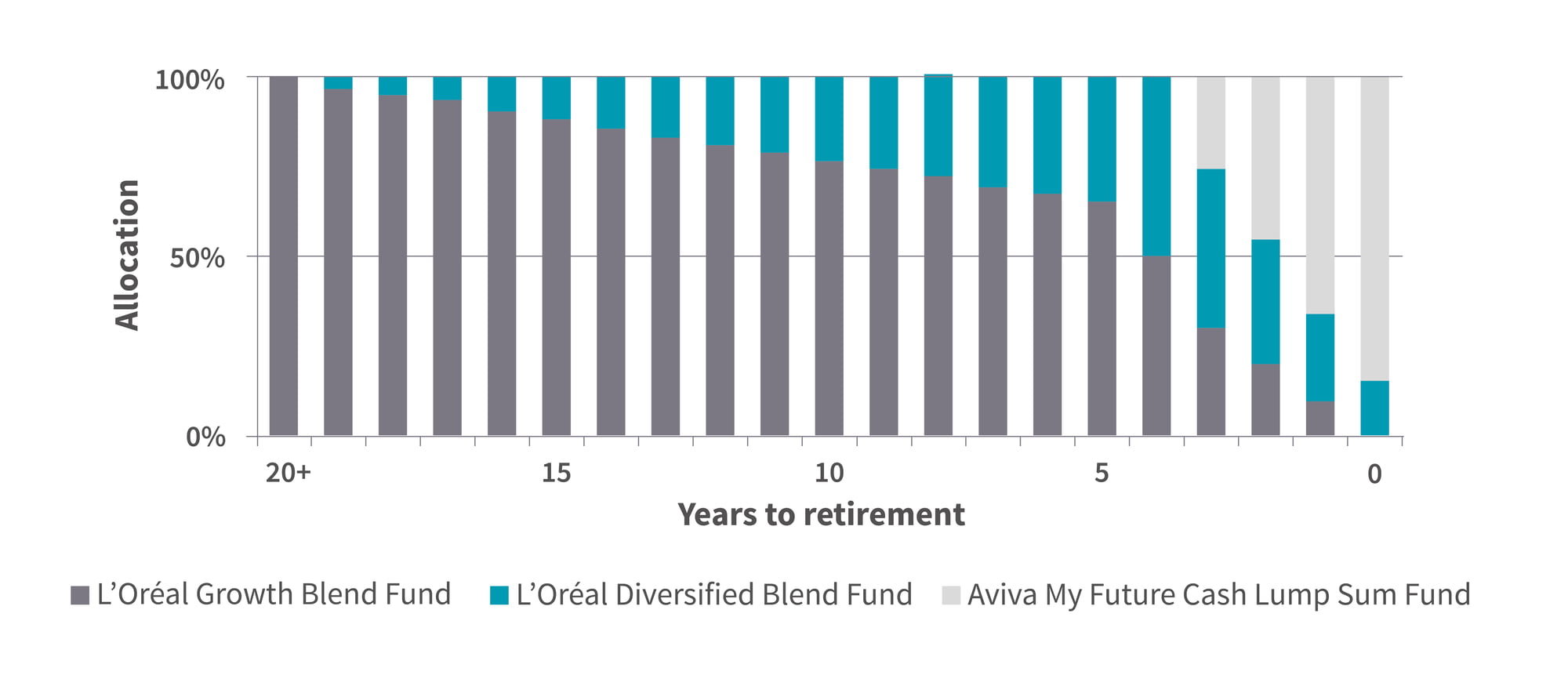

The default arrangement, the L’Oreal – Target Cash Lump Sum Strategy is set out below:

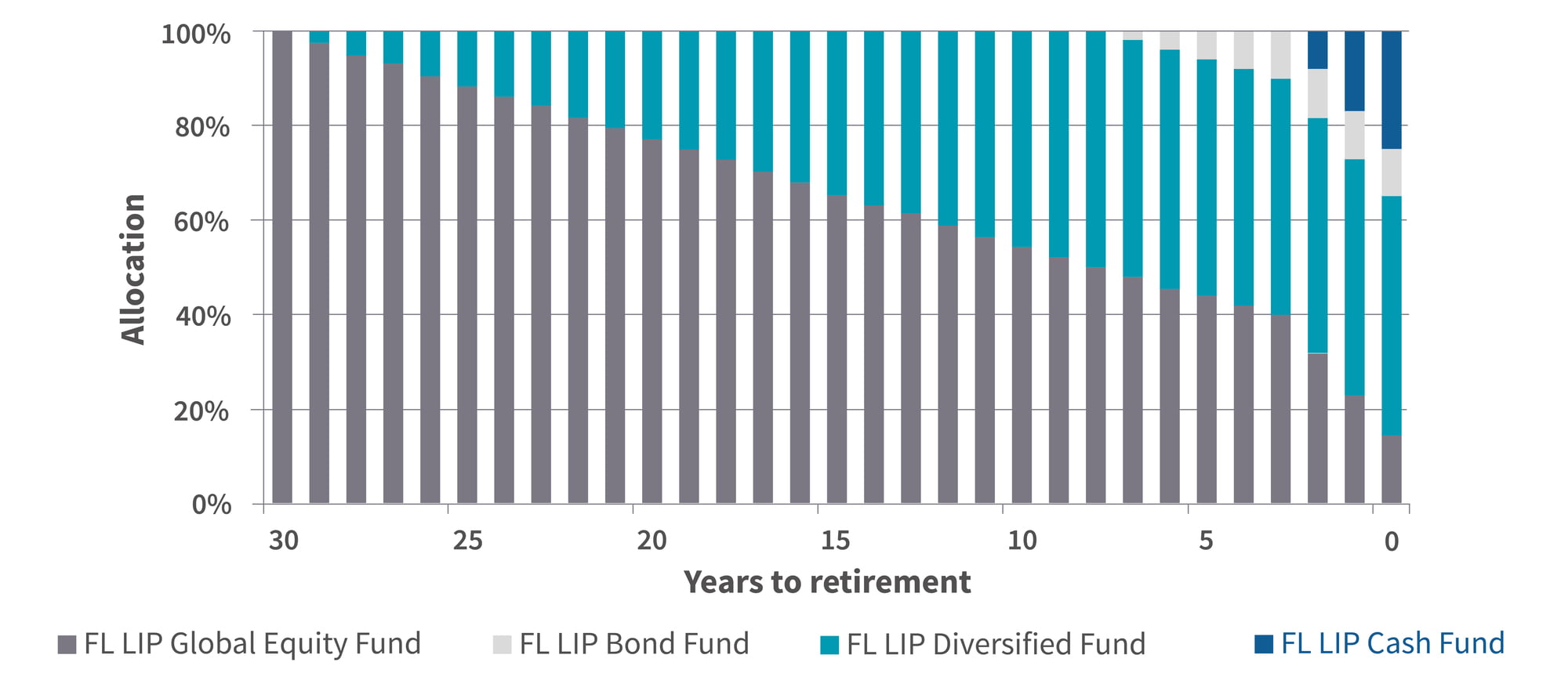

The objective of the default investment solution is to provide an appropriate investment strategy for members who do not wish to make an investment choice for themselves. Up until 20 years from a member’s planned retirement date, the default investment solution aims to help the pension savings grow by investing primarily in shares (also known as equities). The value of savings will fluctuate (increase or decrease) on a daily basis as a result of the performance of the funds used in the growth phase. However, the design of this phase of the programme seeks to limit the likelihood of savings experiencing large fluctuations in value.

In the 20 years leading up to a member’s retirement date, savings are gradually moved into lower risk investments, such as fixed interest and money market investments. This aims to reduce the risk of savings falling in value as members approach their planned retirement date. This is likely to produce lower rates of return.

There is also an alternative default option which has been made available to self-select members as a result of fund suspensions.

For some members who self-select their own funds, there has been a circumstance in which some cash funds have temporarily become a member’s default fund. This has been triggered by the self-select Property fund being suspended to new monies and withdrawals.

For self-select members that had elected to pay regular contributions into the Aviva Pension Property fund, these ongoing contributions are now being re-directed to the Aviva Pension Cash fund for a period of time, thereby making the Aviva Pension Cash fund an additional default investment option.

When the situation arose, Aviva wrote to affected members informing them of the fund closure / suspension and that contributions have been redirected, inviting them to make an alternative fund selection if they wish. When the suspended fund re-opens, Aviva will write to members to inform of the options available to them with regards to re-directed ongoing contributions and cash accumulated in the respective cash funds.

While the Trustees do not believe the respective cash funds are suitable as long-term investments given the limited growth potential and exposure to inflation risk, the Trustees believe that the cash funds are suitable temporary default solutions for the impacted self-select members in the short-term.

In addition to the default the members can choose from a range of 12 self-select fund options.

There is also an alternative lifestyle that members can invest in, known as the L’Oreal Adventurous Strategy. The building blocks of the L’Oreal – Adventurous Strategy are the same as the default strategy but a higher level of risk is targeted earlier on in the glidepath and drawdown is targeted at retirement instead of cash.

This Appendix is for the Mott MacDonald Group Section of the Aviva Master Trust. The Trustees have taken advice from Lane Clark & Peacock LLP (LCP) on the suitability of the investment strategy for this section.

The main investment objectives are to provide members with access to:

A default option has been selected for the Mott MacDonald Group Section, and has been designed to be suitable for a typical member. The default has been chosen taking account of:

The default investment strategy targets income drawdown at retirement which is the retirement option most members are likely to take. This strategy aims to provide strong growth in early years when members can take on more risk. The strategy then aims to reduce investment risk closer to retirement but maintain a reasonable level of growth consistent with a drawdown strategy. The strategy consists of four white labelled funds, each determined by the underlying asset classes. The strategy allocation is shown in the chart below:

In addition to the default the members can choose from a range of self-select fund options.

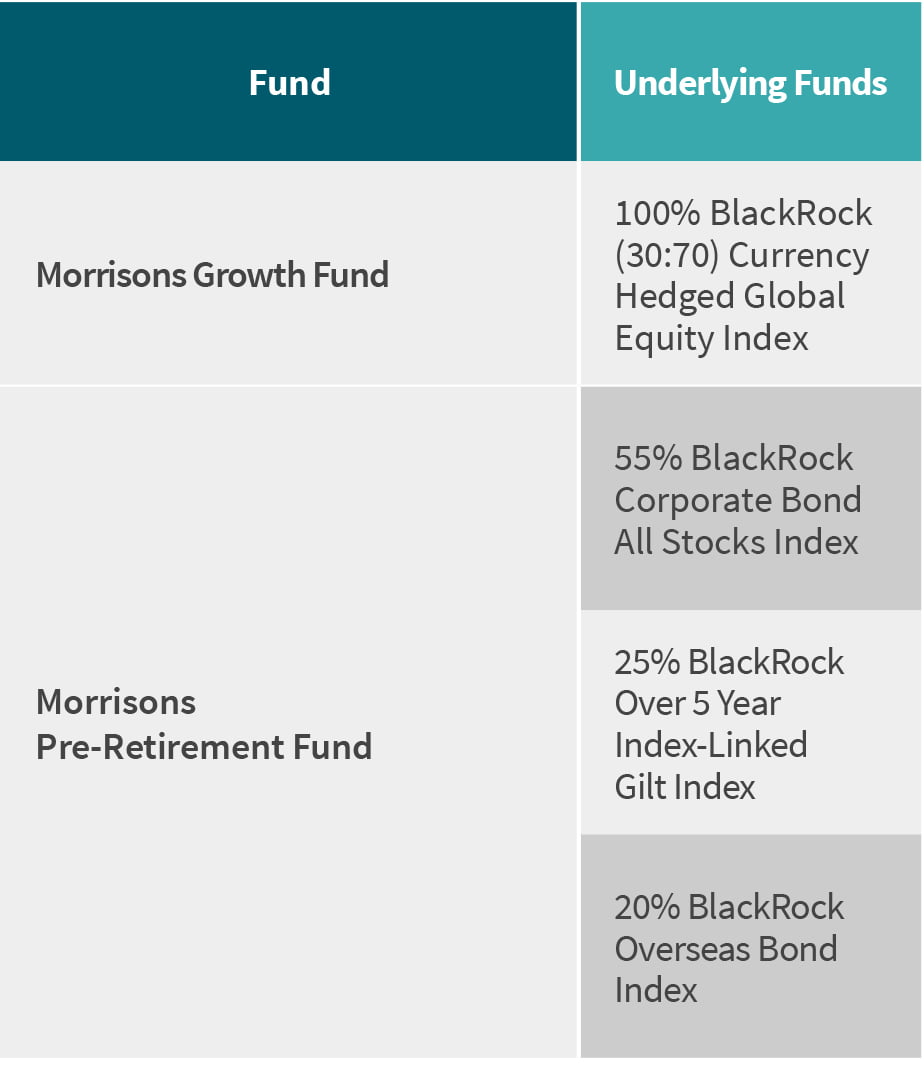

This Appendix is for the WM Morrison Supermarkets Section of the Aviva Master Trust. The Trustees have taken advice from Lane Clark & Peacock LLP (LCP) on the suitability of the investment strategy for this section.

A default option has been selected for the WM Morrison Supermarkets Section and has been designed to be suitable for a typical member. The default has been chosen taking account of:

Following advice provided by LCP on 13 July 2020, it was agreed that the default strategy should continue to target cash withdrawal. This advice was based on summary membership information provided by Aviva covering the period up to 31 March 2020. Analysis of this information continues to suggest that most members expected to retire within the next 10 years will have a projected pot of less than £30,000 and evidence from other DC schemes suggested that pension pots of this size are more likely to be taken entirely as cash by members at retirement. In addition, the analysis showed that the membership is likely to have a relatively high-risk tolerance, because of the younger overall age profile and small pot sizes / average salaries.

There are two white-labelled funds used in the default strategy; the Morrisons Growth Fund and the Morrisons Pre-Retirement Fund. The underlying fund composition of these funds is shown in the table below:

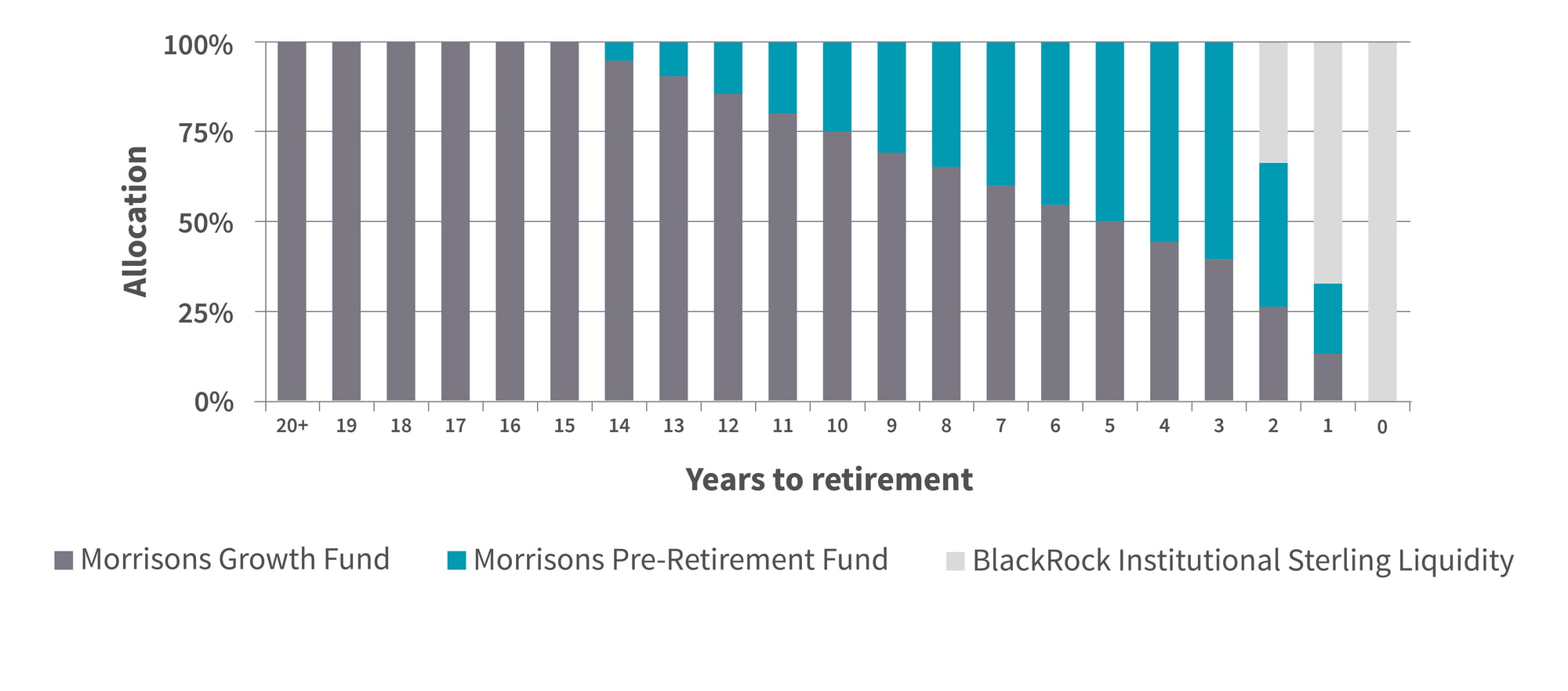

The default lifestyle allocation is shown in the following chart:

The Morrisons Governance Group decided that members would be able to select from the full self-select fund range as governed by the Aviva Master Trust Trustees; no bespoke self-select fund range was put in place, other than to exclude the components of Aviva’s “off-the-shelf” lifestyle strategies from the self-select fund range.

This Environmental Social and Governance (“ESG”) Policy Statement (“the Policy”) has been prepared by the Trustees of the Aviva Master Trust (“the Scheme”) to set out their views on ESG factors (including climate change). It considers how they are addressed whilst meeting the overall objectives of the Scheme’s investment strategy, as set out in the Statement of Investment Principles (“SIP”).

Responsible Investment is the term that the Trustees use to define an approach to investing that aims to incorporate ESG factors into investment decisions, to better manage risk and generate long-term, sustainable returns for members of the Scheme over the time horizons applicable to their membership.

The purpose of the Policy is to sit alongside the Scheme’s SIP, formalising the Trustees’ beliefs on ESG factors as discussed with their legal and investment advisors. The Policy provides a reference point for the Trustees for incorporating ESG factors into investment decision making. It covers those factors that are considered to have a financial impact on investment values, but not non-financial ones such as members’ ethical views.

The Scheme is designed for multiple employers, but delivered under a single trust arrangement and governed by a Trustee Board investing on behalf of members.

As part of their duties, which includes a comprehensive approach to risk management, the Trustees recognise the need for the Scheme to be a long-term, responsible stakeholder.

By taking an active approach to include ESG factors in investment decision making, the Trustees believe they will reduce overall investment risks whilst generating sustainable investment returns.

The Department for Work & Pensions has also expanded the scope of regulations to improve disclosure of Trustees policies on factors financially material to their investment decision making, including ESG factors and climate change. From 1st October 2019, the Trustees are required to include in the SIP their policies on how they take account of these factors. The SIP must also be published online. From 1st October 2020, the Trustees must prepare an annual implementation statement to communicate to members how, and the extent to which, these polices set out in the SIP have been followed during the year.

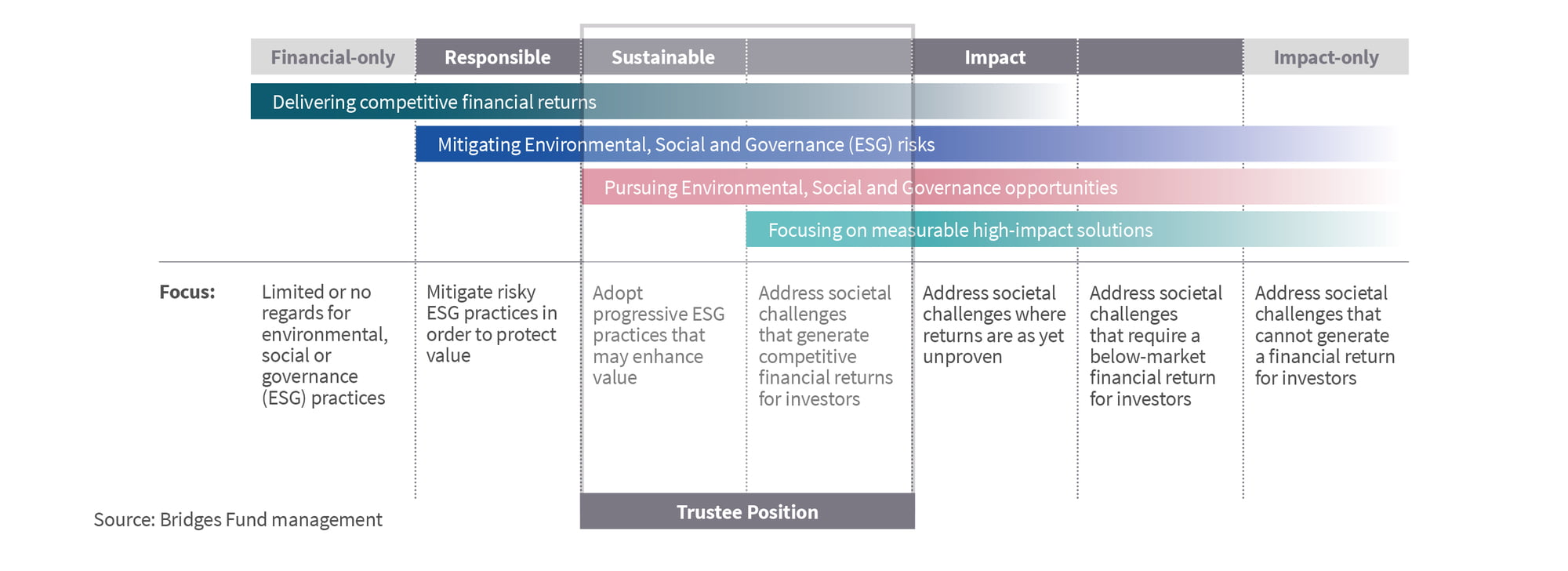

At a meeting on 30th April 2019, the Trustees, with support from their legal and investment advisors, discussed their beliefs in relation to ESG. This included the completion of a questionnaire which captured their views about a set of ESG statements and then mapped the responses against the Bridges Spectrum of Capital (a widely-used industry benchmark for aligning investment beliefs to various approaches to ESG investing). The illustration below sets the different approaches that can be taken.

Following discussions and a review of their responses to the questionnaire, the Trustees agreed that their aspiration was for the Scheme to pursue a “sustainable” investment approach that integrates ESG in investment decision making in order to generate more sustainable long-term investment returns. The Trustees also agreed that the Scheme should seek to invest in a way which is likely to generate a positive and measurable environmental or societal impact whilst generating competitive financial returns. The Trustees’ position is indicated on the Bridges Spectrum of Capital below.

The Trustees have considered and discussed ESG to establish their beliefs to help underpin the Trustees’ decision making. The following represent a consensus of the beliefs held by the Trustees:

The Trustees are working with their advisors and Aviva (as sponsor and provider of the investment platform) to determine how to implement these beliefs most appropriately within the Scheme’s investment strategy.

The Trustees decide the range of funds to be offered within the Scheme and the design of the default investment option.

With regards to the design of the default investment option, the Trustees should ensure that the funds making up the default investment option integrate ESG into the investment decision making process where permissible within applicable guidelines and restrictions. Furthermore, the Trustees should consider offering a lifestyle option comprised of specialist funds which invest according to enhanced sustainable and/or responsible investment themes only, for those members seeking further integration.

The Trustees should ensure that all funds available through the Scheme have considered ESG and have a clear approach and framework for managing these factors. The Trustees should also offer specialist funds which invest according to enhanced sustainable and/or responsible investment themes for the major asset classes where available, as self-select specialist funds are available for members.

In appointing and reviewing the Scheme’s asset managers, the Trustees, with the assistance of its advisor, should consider their approach to ESG.

The Trustees will implement the policy through the following steps:

The Trustees will monitor the Scheme’ assets against this Policy on an ongoing basis, with the assistance of its investment advisor. The development of the Policy is viewed as an ongoing process, with the Trustees reviewing the Policy periodically in line with the SIP. When reviewing the Policy, the Trustees will take account of any significant developments in the market.

In order to further formalise the ESG integration alongside the broader risk management framework, the Trustees will update the SIP when they are comfortable that they have fully addressed this topic.