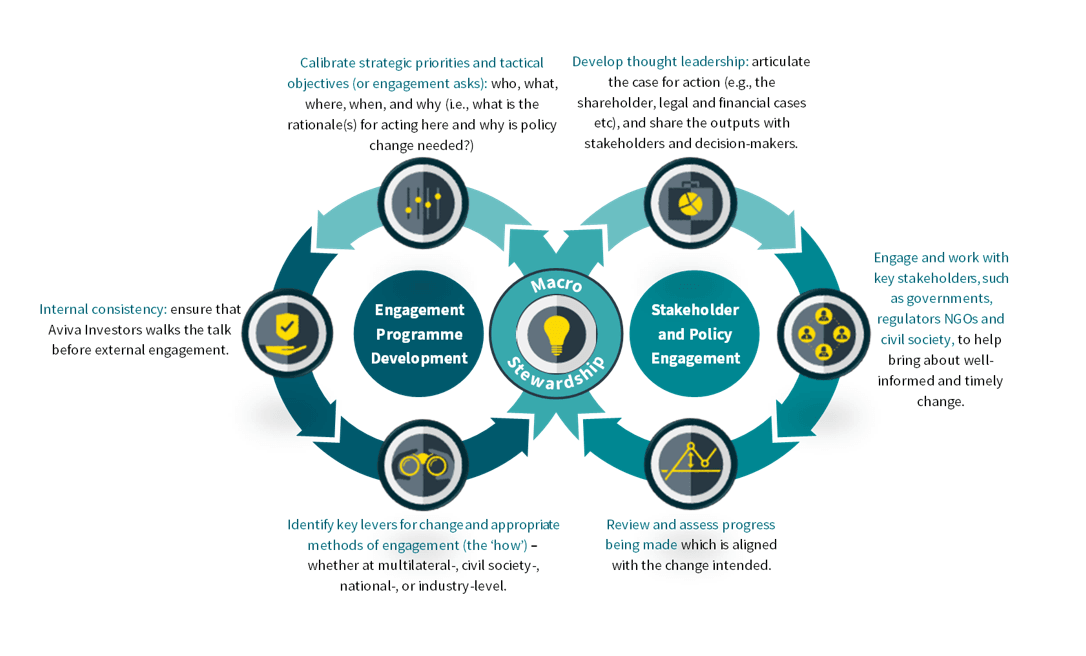

Macro stewardship

Macro stewardship activities depict firm level stewardship activities, not Fund level.

As long-term investors, we recognise that we do not operate in a vacuum. Feedback loops exist between our investment activities and the real world upon which we rely to deliver long-term, risk-adjusted returns. This means that all our investments have an impact, whether positive or negative, on the environmental, societal, and financial systems upon which the assets we invest in rely.

These real-world systems can affect the overall risk and return profile of capital markets, and therefore financial market participants and, by extension, the best interests of the clients whose capital we are entrusted to manage. We believe it is in our clients’ long-term interests to take effective action to ensure these systems have integrity, are resilient and function sustainably and fairly. When markets operate in such a way that leads to a sub-optimal outcome for society or the environment or destroys value, they may be said to fail. Unpriced negative externalities, such as companies not having to reflect the impact their carbon emissions have on climate change in their cashflows and on their balance sheets, fail to reflect their “true” cost or fundamental value and the true extent of the risk. There are a number of different types of market failure, but all undermine the ability of markets to price assets in line with the true nature of their risk and fundamental value. Left unchecked, market failures can increase systemic risks that can disrupt the stability of the market and threaten investment performance and long-term returns. This could ultimately cause the breakdown of the entire system, which would affect all asset classes, in all sectors and geographies.

Each of the Sustainable Development Goals (SDGs) can be said to be representative of one or more market failures. Collectively, the potential failure to deliver the SDGs represents a risk to the stability and integrity of financial markets, with concurrent risks for market participants and our clients. As such, we believe we have a duty to act to highlight and seek correction of market failures and systemic risks as part of our obligations to our clients and to the integrity of markets.

Our firm level macro stewardship work is separate from our risk management activities and micro stewardship activities. We define the practice of macro stewardship as “taking action to accelerate systemic change with the intention of seeking correction of market failures and mitigation of systemic risks consistent with our view of the long-term best interests of clients and market integrity.”

This requires engaging with policymakers, regulators and other key decision-makers who shape the markets within which we operate. Through targeted programmes of engagement that intentionally and proactively identify policies and practices to mitigate systemic risks, we seek to contribute to the stability of the environmental, societal, and financial systems upon which the assets we invest in rely.

Correction of market failures cannot be achieved by market participants alone, as the levers to do so are in the hands of policymakers and regulators. But nor is it something that policymakers and regulators can do effectively or efficiently in the absence of multi-stakeholder engagement. Identifying and establishing regulatory systems and policy interventions to correct material market failures and foster sustainable, fairer, and more resilient capital markets therefore can therefore be enhanced by robust feedback loops between investors and policymakers.

The enactment of policy and regulatory shifts presents threats and opportunities for investors, with winners and losers arising from change.

Those who fail to identify and respond to future transitions in the policy and regulatory environment risk missing long-term investment opportunities presented by companies that are well-positioned for the changing environment.

Watch our video interview with

Watch our video interview with Sophie English, Macro Stewardship Analyst at Aviva Investors.

Such a failure in the predictive power of investors is a prime example of a market inefficiency, and often results in the mispricing of capital. As such, macro stewardship, and our work to bring about these corrections, is not only a key mechanism through which we aim to deliver sustainable outcomes, but also better connects us with the likely scale and pace of change. We believe this can provide an information advantage, which in turn enhances our ability to exploit market inefficiencies. As such, our work helps generate positive feedback loops between our investment activities and the environmental, societal, and financial systems upon which our clients depend.

Seeking international financial system reform to unlock private capital and deliver global climate goals

The 28th annual United Nations (UN) Conference of the Parties (COP28) was held in Dubai in November and December 2023. COP28 saw the 198 “parties” (countries) that signed the UN Framework Convention on Climate Change (UNFCCC) in 1992 come together to discuss progress made on climate action. The UNFCCC commits the countries to work together to stabilise emissions “at a level that would prevent dangerous anthropogenic (human-induced) interference with the climate system.” Later COPs have added further agreements to the global climate action ecosystem, most notably the Paris Agreement, agreed at COP21 in 2015, in which 196 countries agreed to limit emissions to levels that would keep global temperatures increases “well below” 2 degrees Celsius above the pre-Industrial Revolution average, while pursuing efforts to limit warming to as close to 1.5 degrees Celsius as possible. The key outcome of 2022’s COP27 for Aviva Investors was a recommendation for financial system reform to deliver the investment necessary for the energy transition.

Throughout 2023, leading up to COP28, it was clear that urgent and significant progress needed to be made on the crucial question of how the world finances the global transition, for which we need to harness $4 to $6 trillion of investment per year. This climate finance gap threatens the implementation of global climate goals, such as the Paris Agreement, which poses a financial risk to all asset classes in all geographies. A near 3°C global temperature increase could hit 18% of global GDP20 and therefore threaten the integrity of the market and potential investment returns.

As part of the first Global Stocktake (a process set out under the Paris Agreement to assess the global response to climate change every five years), climate finance continued to be a key theme at COP28.

20 Swiss Re (April 2021) The economics of climate change: no action not an option

To set out our thinking about how this question might be effectively answered, we launched our new climate finance report, The Tipping Point for Climate Finance, in November ahead of attending COP28 in Dubai. This report set out four clear steps for the Global Stocktake in aid of the creation of a transition-plan ecosystem connecting all levels of the global economy:

Create an implementation vision to make all financial flows consistent with Article 2.1.c of the Paris Agreement, which can be led by the creation and implementation of national transition plans.

Change economic fundamentals to ensure Parties make not only essential and urgent enhancements to Nationally Determined Contributions (pledges made by countries under the Paris Agreement to reduce their emissions and adapt to the impacts of climate change) but respond with a clear implementation plan – a national, whole-of-government transition plan with annual reporting on progress.

Transition the international financial architecture with a detailed regulatory vision to align the regulation and supervision of finance with the ambitions of Parties. All bodies within the international financial architecture should respond to the signals sent by government stakeholders in signing up to global climate and nature goals by creating their own institutional transition plans, setting out how their work will transition to take account of the global commitment to net zero.

Build or mandate institutions to provide clear guidance for national and financial architecture transition plans, along with an annual synthesis report that monitors implementation and supports iterative, dynamic, and responsive plans that evolve with the accelerating a just transition.

While at COP28, we extensively engaged with key policymakers and negotiators during the conference to advocate for the consideration of meaningful financial system reform, including within the outcome text. We attended the 4th Public-Private Sector Climate Finance Dialogue, in which negotiators and private finance actors explored how private finance can be maximised in support of the Paris Agreement goals. There, we introduced our report’s proposals, including national transition plans for the implementation of NDCs and multilateral institution transition plans to set out how their mandates and practices will evolve.

We were also invited to present our thinking to the finance negotiators at the 8th Technical Expert Dialogue for the New Collective Quantified Goal on climate finance. We took part in high profile events covering private and public finance related to transition planning, including a Glasgow Financial Alliance for Net Zero (GFANZ) roundtable with the Financial Stability Board and global regulators, and a panel hosted by the Network for Greening the Financial System (NGFS). During these events, we highlighted the need for mandatory transition plans for companies globally and for alignment on metrics, which should then support transition plans at the level of countries and the international financial architecture.

We were pleased to see financial system reform reflected strongly in the COP28 outcome text, particularly the call on countries to strengthen their regulatory, policy and incentive frameworks in order to unlock private finance in support of the transition and to work together to reform the international financial architecture.

While we were pleased to observe this progress, there is still a considerable way to go if we are to achieve the changes that we believe are needed, and we will therefore continue to advocate in the multilateral climate finance process. This includes inputting to sustainable finance multilateral processes, such as the ongoing dialogue on the New Collective Quantified Goal – a new global climate finance goal which will be set by the end of 2024 from a floor of $100bn per year taking into account the different needs and priorities of emerging markets and developing economies - and continuing to advocate for national transition plans to shift economic fundamentals to enable the global transition to a net-zero economy. We will also continue to engage with national and international policymakers on the mobilisation of climate finance for emerging markets and developing economies to deliver a just and orderly transition to net zero in the Global South.

Strengthening UK net zero policy to drive investment growth in low carbon sectors and support economy-wide decarbonisation

Achieving net zero emissions by 2050, as required by the UK’s Climate Change Act, is not only an environmental necessity, but also an essential transition for the UK’s future economic prosperity and the stability of its financial system. If we are to reduce risk to financial stability and realise what the HM Government-commissioned ‘Mission Zero Review’ has described as “the growth opportunity of the 21st Century”, the transition must take place in a timely and orderly fashion. However, in order to do so, a significant increase in low-carbon investment is required this decade to keep global temperature rises within the goals set in the Paris Agreement and for the UK to realise the economic opportunity presented by the net zero transition. The UK Government estimates that an extra £50 to £60 billion capital investment will be required each year from the late 2020s and throughout the 2030s21, which cannot be met by public finance alone.

As such, cross-economy and sector-specific policy levers are required to improve market conditions and mobilise greater private capital into low-carbon investment opportunities. This in turn will help to support economy-wide decarbonisation, which will help to preserve the integrity of the market and enable better potential investment returns.

Throughout 2023, after creating a new Head of Climate Policy role, we developed a new engagement programme focused on developing our public policy positions across key sectors of the economy to de-risk and drive private sector investment growth into low carbon technologies, infrastructure, and businesses to support economy-wide decarbonisation. As an early output from the creation of this role, Aviva Investors began developing a UK Low Carbon Investment Policy Roadmap in 2023, summarising the most important policy solutions over the next five years to unlock private low carbon investment on a sector-by-sector basis. This Roadmap, which will be published during the course of 2024, received input from investment colleagues from across the business and key external real economy businesses.

21 Mobilising Green Investment - 2023 Green Finance Strategy (publishing.service.gov.uk)

Our external work in 2023 aimed to drive public policy change that will unlock private low carbon investment across all key sectors of the UK economy, thereby facilitating Aviva Investors’ gathering of green assets as well as supporting the UK’s and other countries’ transitions to net zero emissions. We attended – and spoke at events - at the Conservative, Labour, and Liberal Democrat Party conferences. At these events, we emphasised the need for public policy interventions and targeted public funding to de-risk and attract private investment into low carbon projects, infrastructure, and businesses at scale across the UK economy. By giving a preview of AI's upcoming Roadmap and our key recommendations, we formed relationships with ministers, shadow ministers and election manifesto drafters to facilitate future dialogues on our public policy proposals.

Looking forward, our upcoming publication due in June 2024, the UK Low Carbon Investment Policy Roadmap, will set out our perspective on key solutions to unlock private investment in low carbon infrastructure and business across eight major sectors of the UK economy following extensive consultations within the business and with external businesses. Using the Roadmap as a foundation, we will engage with the UK’s major political parties to advocate for the inclusion of our key recommendations in their General Election manifestos. This is already underway with the Roadmap feeding into Mark Versey’s input to the Department for Energy Security and Net Zero’s Net Zero Industry Council and Amanda Blanc’s ongoing participation in the Labour Party’s National Wealth Fund Taskforce. After the General Election – which will be in January 2025 at the latest – we will support the next Government by engaging with new ministers and parliamentarians and responding to impactful policy consultations and parliamentary inquiries to help shape investment-relevant policy decisions.