Chair’s Annual Statement - Aviva Master Trust (‘the Scheme’) For the Scheme Year ended 31 March 2020

This Statement has been prepared by the Trustees of the Scheme (“the Trustees”) in accordance with Regulation 23 of the Occupational Pension Schemes (Scheme Administration) Regulations (“the Administration Regulations”) 1996 (as amended). It describes how the Trustees have met the statutory governance standards in relation to:

The Trustees are pleased to confirm that the Scheme received authorisation from the Pensions Regulator in August 2019 and as an authorised Master Trust is now subject to the ongoing supervision of the Pensions Regulator. The Trustees are committed to running the Scheme effectively and efficiently so that it can deliver the best possible outcomes for members. The Trustees undertake continual development and improvement to demonstrate the adoption of rigorous governance standards that are in line with industry best practice. This is borne out by the accreditation already achieved with the Type 2 Audit and Assurance Faculty (AAF) 02/07 audit relating to the Scheme Year.

From early March 2020, Aviva offices were closed as part of the lockdown measures that were required across the UK. Aviva has moved its operational capacity to home working, through provision of laptops, screens and peripherals to future home workers as well as implementing a significant increase in the capacity of Aviva’s Virtual Private Network (VPN). In addition, telephony capability has been provided to the member helpline staff. This has meant that administration can be provided by staff working from home.

The Trustees have met regularly with Aviva (on a virtual basis), with additional specific investment meetings, to discuss and review COVID-19 measures and risks and to ensure that the Scheme continues to comply with guidance from the Pensions Regulator. This has involved testing and challenging administrators’ and advisers’ plans and responses to COVID-19 not only in terms of current impacts but also testing contingency plans in the light of further developments (e.g. staff shortages). This has demonstrated that Aviva has been largely successful in its response to the pandemic and its contingency planning. Aviva has moved staff to working from home without a significantly adverse impact on service and has adapted to the Trustees’ requirement for additional management information and meetings. There have been no issues or concerns relating to how the Scheme's advisers have responded to COVID-19.

The Trustees have also reviewed their own effectiveness and delegation processes in the light of COVID-19 and made appropriate changes to ensure that they could continue to operate fully and effectively at all times.

The Trustees and Aviva have provided a number of communications to members and employers, providing assistance, guidance and reassurance in relation to the potential impact of COVID-19.

The Trustee Board for the Scheme Year ending 31 March 2020 was made up of Colin Richardson representing PTL (Chair), Rebecca Cooke, Anne Hunt and Jonathan Parker. On 11 May 2020, Anne Hunt resigned from the Trustee Board and was replaced by Elizabeth Renshaw-Ames and Priscilla (known as Tilly) Ross.

On 18 May 2020, Elizabeth Renshaw-Ames was appointed as the new Chair of the Trustee Board. Colin Richardson stepped down as Chair and remained a Trustee.

The Scheme provides retirement benefits for employees and former employees of a number of employers. Although the Scheme offers a range of investment options for all its members, it has investment options available for members who do not make a choice about how their savings in the Scheme are invested, including those automatically enrolled in the Scheme by their employers. These are referred to as default investment options in this Statement and are the Scheme’s “default arrangements” for the purposes of the Administration Regulations. Some members actively choose to invest in the default investment options as they match their requirements in terms of risk and returns; however, most members whose savings are invested in the default investment options do not make an active investment choice and are therefore placed in these options.

The Trustees have regard to the relative investment return and risk that each asset class is expected to provide. The Trustees are advised by their independent professional advisers on these matters, who they deem to be appropriately qualified experts. However, the day-to-day selection of investments is delegated to the investment managers.

The Scheme provides a standard default investment option and an alternative default investment option. These options are available to employers who do not wish to implement a bespoke default investment option to use in respect of their employees.

The overarching objective of the Scheme’s standard and alternative default investment options is to deliver long term positive returns, after charges, taking account of a number of different risks.

The standard default investment option for the Scheme Year ending 31st March 2020 was the Aviva My Future strategy.

The Aviva My Future strategy invests in the My Future Growth Fund until 15 years before a member’s selected retirement date and then it transitions in stages towards the My Future Consolidation Fund at the member’s selected retirement date.

On 18 July 2019 the Trustees took the decision to offer the Aviva My Future Focus strategy as an alternative default investment option that would be suitable for members. The background to this decision is as follows:

The Trustees, in conjunction with Aviva, commenced a detailed review of the Aviva My Future Plus strategy in December 2018. This review encompassed:

the manager of the investment strategy

the design of the strategy (including the glidepath)

the asset allocation process and the asset classes used

the integration of Environmental, Social and Corporate Governance (ESG) factors

annual management charge for members investing in the strategy

On 30 June 2020, following a further investment review, the Trustees decided to change the standard default investment option of the Scheme to the Aviva My Future Focus strategy. At this point, it was also decided that the Aviva My Future strategy continued to be suitable for members and would therefore be retained and become the alternative default investment option for the Scheme.

Where employers use a bespoke default investment option (i.e. one designed specifically for their section of the Scheme), the employer and the Trustees receive advice on the suitability of that bespoke default investment option. These investment advisers are appointed by the Trustees.

The bespoke default investment options in place at the end of the Scheme Year (and their associated objectives) are listed in Appendix 2 of the Statement of Investment Principles. No changes have been made to the structure of the bespoke default investment options during the Scheme Year.

The Scheme incorporates additional default investment options created following the suspension of certain property funds. The overarching objective of these additional default investment options is to provide members with a secure short-term investment for their contributions. The creation of these additional default investment options followed a review by the Trustees, in conjunction with Aviva and the Trustees’ investment adviser, in response to the suspension of the property funds resulting from their independent valuers applying a ‘material uncertainty clause’ on the valuation of the properties held by the funds following the impact of COVID-19. In this context, the Trustees decided, supported by a recommendation from their investment adviser, to direct members' regular contributions into a cash / money market fund from 20 March 2020.

The Scheme also incorporates additional default investment options created following the transfer of benefits from certain single employer schemes into the Scheme. The overarching objective of these additional default investment options is to provide members with a risk and return profile and objective that is consistent with the fund from which they were mapped. These additional default investment options were established before the start of the Scheme Year.

Further information on these additional default investment options is included within the Statement of Investment Principles (SIP) which is attached to this Statement as Annex 1.

The Trustees review each default investment option regularly and, as required by law, at least once every three years to ensure that the default options remain suitable for the relevant membership. These reviews involve assessing the investment performance of the default investment options against their benchmarks, the extent to which investment performance is consistent with their aims and objectives in respect of those arrangements and the prospective risk and returns profile for each option. These reviews also consider the membership demographics of the section(s) of the Scheme to which they relate to ensure suitability for the members concerned.

The Aviva My Future default investment option was last reviewed on 21 March 2018. The next review of the Aviva My Future default investment option is due to take place no later than 21 March 2021, although an earlier review may take place.

The Aviva My Future Focus default investment option was last reviewed on 18 July 2019 when it was established as an alternative default investment option. The outcome of this review was described earlier within this Chair’s Annual Statement. The next review of the Aviva My Future Focus default investment option is due to take place no later than 18 July 2022 although an earlier review may take place.

The bespoke default investment options are as follows:

None of the bespoke default investment options were reviewed in the Scheme Year ended 31 March 2020.

The default investment options for the Morrisons section and the Mott MacDonald section were reviewed and re-approved by the Trustees (having taken advice from LCP on their continued suitability) on 12 August 2020. Further detail of the review will be incorporated within the Chair’s Annual Statement for the year ending 31 March 2021. The default investment options for these sections will be reviewed again by the Trustees by 12 August 2023 or without delay after any significant change in investment policy, if sooner.

The default investment options for the C&J Clark section and the L’Oréal section will be reviewed by the Trustees by 1 August 2021 and 1 March 2021 respectively or without delay after any significant change in investment policy, if sooner.

As stated earlier, the Scheme also incorporates a number of additional default investment options which were created following the transfer of benefits from certain single employer schemes into the Scheme and following the suspension of certain property funds. The Trustees have determined that these funds are suitable additional default investment options for the impacted self-select members. The Trustees will continue to regularly review this assessment. These additional default investment options are shown below:

In addition to the strategic triennial reviews described above, Aviva provides the Trustees with quarterly investment reports which allow the Trustees and their investment adviser to regularly monitor the performance of the investment funds offered by the Scheme, including those which make up the default investment options. Fund performance was reviewed at each Trustee meeting in the Scheme Year. The Trustees’ investment adviser, Isio, advise the Trustees on the investment fund performance, the continued suitability of the standard default investment option and the alternative default investment option.

A review of the appropriateness and performance of the self-select funds was carried out by the Trustees on 6 February 2020 having taken advice from Isio. It was agreed that the Scheme’s existing self-select fund range continued to be appropriate for the Scheme.

The principles governing how decisions about investments must be made are detailed in the Scheme’s Statement of Investment Principles (“SIP”). The SIP sets out the Trustees’ investment aims, objectives and policies for the Scheme’s default investment options and is prepared in accordance with regulation 2A of the Occupational Pension Schemes (Investment) Regulations 2005. In particular, it covers:

A copy of the SIP as at 28 September 2020 is attached to this Statement as Annex 1.

For each employer using a bespoke default investment option in relation to their section of the Scheme, a bespoke appendix to the SIP is maintained. The bespoke appendices to the SIP are included with the SIP attached to this Statement as Annex 1.

“Core financial transactions” include (but are not limited to):

Receipt and investment of contributions in the Scheme

Transfers of assets relating to members into and out of the Scheme

Transfers of assets relating to members between different investments within the Scheme

Payments from the Scheme to, or in respect of, members.

During the Scheme Year, the Trustees received assurances from the Scheme’s administrator (Aviva) and have taken steps to ensure that adequate internal controls were in place to ensure that “core financial transactions” of the Scheme were processed promptly and accurately. The Trustees have ensured this by:

The Trustees are pleased to confirm that there were no material administration service issues, including relating to the processing of core financial transactions, reported to or picked up by the Trustees during the Scheme Year. The Trustees were informed of a break in unit reconciliations affecting a small portion of the employer sections administered on the NGP Platform. This was rectified by Aviva upon identification and additional controls were put in place to prevent any recurrence. There was no adverse impact to any members and as such the Trustees do not regard this issue as material in respect of the requirements to ensure that core financial transactions are processed promptly and accurately.

The Trustees worked closely with Aviva at the start of the pandemic to agree priority servicing to core financial transactions as well as maintaining full telephony support for members. The Trustees held weekly calls with Aviva to monitor the service being provided by Aviva and to understand the plans in place to manage any on-going impact of the pandemic.

The transition period from office working to remote working had a small impact on some demand SLAs as staff were being equipped to work effectively from home, which was to be expected given the exceptional circumstances. The Trustees are aware that service pipelines are now reducing due to reduced customer demand and that this remains under constant scrutiny. The Trustees do not regard this drop in the SLA as material in respect of the requirements to ensure that core financial transactions are processed promptly and accurately.

Aviva is mindful of any potential change in customer behaviour and the impact to on-going service and this is being monitored closely. The Trustees have agreed the need to assess the COVID-19 SLA performance in context of the circumstances at the present time and the Trustees acknowledge the prioritisation of particular administration tasks. Telephone services for members have been maintained throughout the COVID-19 period.

In accordance with Regulation 25(1)(a) of the Administration Regulations, the Trustees calculated the charges and the transaction costs, borne by members of the Scheme during the Scheme Year. For these purposes, “charges” means “administration charges other than transaction costs, costs relating to certain court orders, charges relating to pension sharing under the Welfare Reform and Pensions Act 1999, winding up costs and costs associated with the provision of death benefits”. “Transaction costs” are those incurred as a result of the buying, selling, lending or borrowing of investments.

The level of charges and transaction costs applicable during the Scheme Year to the Scheme’s default investment options and to all investment options and funds that are not default investment options are shown in Annex 2. For individual members, benefit statements will show the web address where costs and charges information specific to their employer’s section of the Scheme can be found. This can also be found using an internet search engine.

The Trustees can confirm that the charges during the Scheme Year met the statutory charge cap requirement. This requires that charges for "default arrangements" (for the purposes of the Administration Regulations) within auto-enrolment schemes are a maximum of 0.75% per annum of funds under management since April 2015. Legislation does not set a charge cap in relation to self-selected investment funds which are not “default arrangements”.

In accordance with Regulation 25(1)(b) of the Administration Regulations, the Trustees assessed the extent to which the charges and transaction costs referred to above represent good value for members.

The Trustees’ overall conclusion is that on an overall basis the charges and transaction costs represented very good value for members during the Scheme Year.

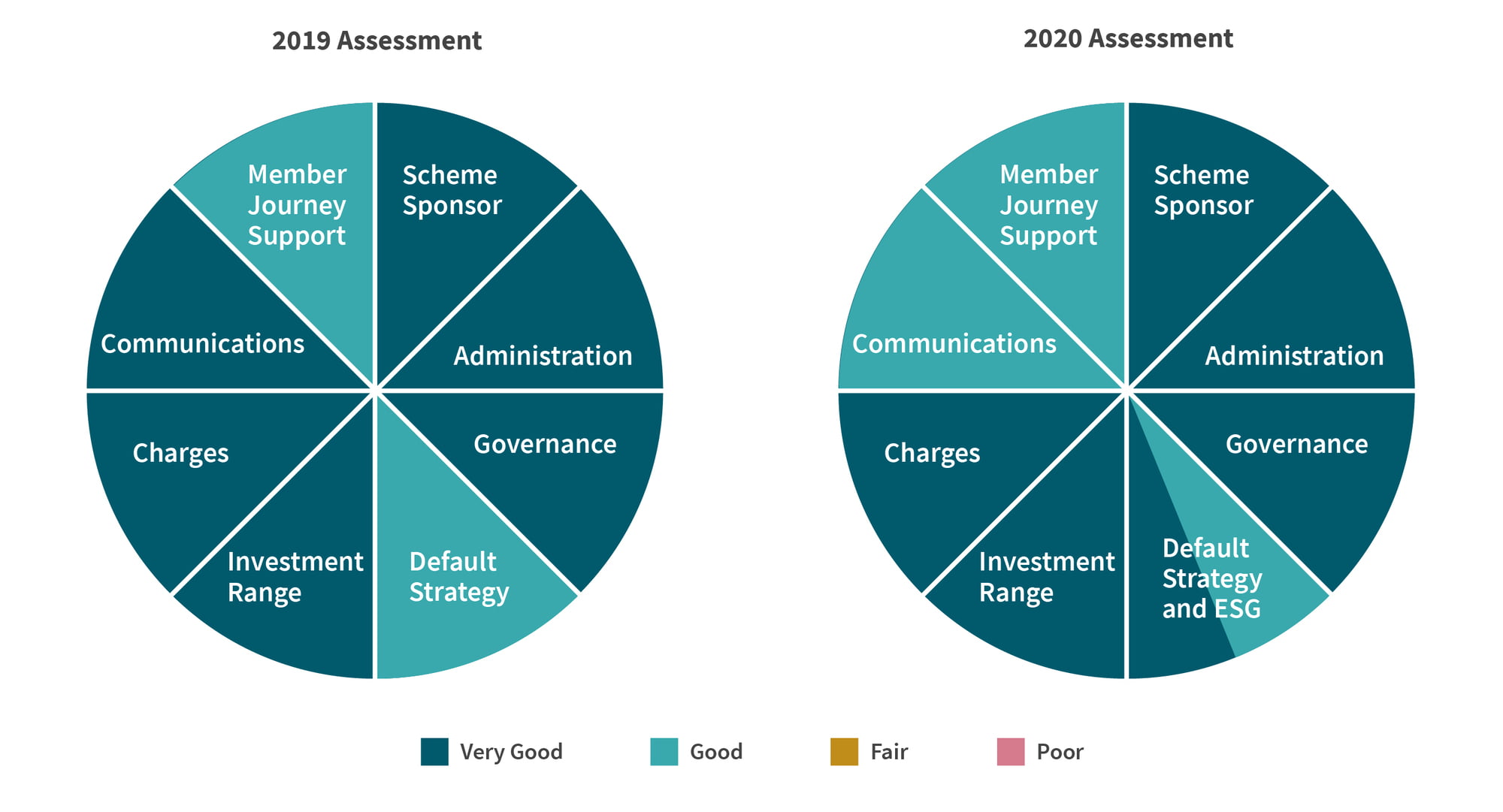

The following charts illustrate how the Trustees came to this conclusion:

In 2020, the Default Strategy & ESG assessment shows 2 ratings, “good” for the Aviva My Future strategy and “very good” for the Aviva My Future Focus strategy

There is no statutory definition of “good value” or specific requirements setting out how value should be assessed. The Trustees take into account Guidance from the Pensions Regulator on assessing “good value” plus deliberations with their adviser this year and in previous years on the areas and method of assessment. The Trustees’ assessment of value for members relating to the Scheme Year included assessing all features and benefits of the Scheme relating to any costs met by Scheme members. The costs met by Scheme members are the charges and transaction costs shown in Annex 2. Consequently, when assessing value for members, it is the absolute level of charges and transaction costs, which includes the costs of the operational and administrative elements of the Scheme, customer services and member communications, that the Trustees evaluated.

Accordingly, the Trustees’ value for members assessment relating to the Scheme Year was carried out by:

During the review of the areas to be assessed, two were changed to better reflect the areas that the Trustees believed to be key. ESG was added as a key consideration of the ‘default investment option’ as the Trustees’ beliefs and views in terms of ESG developed significantly over the Scheme Year and the Trustees are keen to further develop this area with Aviva. The ‘member journey support’ area was modified to reflect the Trustees’ belief that, to support good member outcomes and offer good value for members, the members' full journey should be focussed on and assessed.

The Trustees consider all the areas are vital and did not apply any specific weighting between the 8 areas in their overall assessment of value for members.

The assessment conclusion of the Trustees for each area is shown below. The Trustees assessed each area and then subsequently tested these against independent advice from Isio and debated these with them. Following this process, the Trustees reconfirmed their conclusions which did align with those of Isio.

1. Scheme Sponsor – Trustee Assessment: Very Good – The Scheme Sponsor continues to have strong financial strength and durability to continue to invest and grow in the UK defined contribution market and invest in a range of propositions to enhance the Aviva Master Trust. Through the Trustee and Scheme Strategist meetings the Trustees now also have a close relationship with key members of the Aviva team. The Trustees receive reports on Aviva financial results and strength.

2. Trustee Governance – Trustee Assessment: Very Good – The independent Trustees have a broad knowledge base with many years of experience in the pensions industry covering actuarial, investments, scheme secretariat, legal, auditing, communications, client management and pensions management for both DC and DB Schemes and this is also supported by the governance carried out by Aviva. The introduction of an Investment Sub-Committee and a Risk Sub-Committee has further strengthened the governance oversight. The high levels of governance of the Scheme have also been validated by the AAF 02/07 Audit. The governance has been further enhanced after the end of the Scheme Year with the addition of two new trustees including a new Chair (as described in the introduction and Section 6 (Trustee Knowledge and Understanding)). Following these appointments, the Trustees are undertaking a further review of their governance and establishing additional sub-committees. The Trustees have also been creating a Mission Statement and Strategic Objectives to focus their governance.

3. Default Strategy & ESG – Trustee Assessment: Two results: Good for My Future and Very Good for My Future Focus - The Trustees have chosen to show the two ratings for the two main default investment options – Aviva My Future strategy and Aviva My Future Focus strategy.

During the Scheme Year, the majority of the members' investments were invested in the Aviva My Future strategy which remains a default investment option. Explicit ESG integration will be introduced in the current Scheme Year ending 31 March 2021. This integration after the end of the Scheme Year ending 31 March 2020 is one of the reasons for the rating of “good” rather than “very good” for the year 2019/20, together with the investment mix not being as well diversified as the Aviva My Future Focus strategy.

During the Scheme Year an enhancement was made to the Aviva My Future Focus strategy to increase explicit ESG integration and greater diversification. Both the Trustees and Isio regard these as strong enhancements leading to the rating shown. The ESG integration covers the entirety of equity funds and the majority of the investments. With effect from 30 June 2020, the Aviva My Future Focus strategy has been selected as the Scheme’s standard default investment option in alignment with the Trustees’ ESG Beliefs.

Isio has carried out its annual investment performance review of the default investment options in 2020 and noted that whilst the Aviva My Future Growth fund and the Aviva My Future Focus Growth fund delivered negative returns during Q1 2020 as a result of the impact of the COVID-19 pandemic on the investment markets, they fared slightly better compared to other comparable defaults. This helped underpin the ratings shown. It should be noted that at present the Aviva My Future Growth fund is delivering a positive return calendar year-to-date whilst the Aviva My Future Focus Growth fund is delivering only a marginally negative investment return calendar year-to-date and both have continued to compare well to other similar defaults in the market this year.

The Trustees continue to fully consider both what their beliefs are around ESG and how these should be reflected in the Scheme’s investment strategy.

4. Investment range – Trustee Assessment: Very Good – Appropriate and varied fund range offered to members with the alternative My Future Focus & My Future Lifetime Investment Programmes available to meet the pension flexibilities with the aim of the member achieving their chosen retirement outcome. In addition, an ethically focussed investment strategy, using Aviva’s Stewardship funds, has been added as an option that can be selected by members. Alongside this, the Stewardship funds (5 in total) were added to the self-select range, complementing the existing specialist Ethical and Sharia funds. The self-select range has also been reviewed by Isio and the Investment Sub-Committee in 2020.

5. Charges – Trustee Assessment: Very Good – The Trustees rating reflects Isio’s views, which rated this aspect “Very Good” based on the benchmarking which was carried out. This considered the charges applied by other master trusts in the market, including by the Scheme ‘s key competitors, and commented that they continued to see that the charges quoted by the Aviva Master Trust for schemes are competitive against its peers.

6. Administration – Trustee Assessment: Very Good – The Trustees challenged Aviva through the Scheme Year on its administration processes and reporting. All the Trustees also participated in a site visit. Aviva continues to have tested and maintained strong procedures for cash flow with SLAs in place for money handling as well as an Internal Dispute Resolution Procedure (IDRP) in place, which is reviewed annually, in addition to a standard complaints process. The Trustees and Aviva have worked together to refine the IDRP process to speed up responses when matters arise. Quarterly administration reports are provided to the Trustee Board and these reports are subject to continuous improvements. The high standard of the administration of the Scheme has been further validated by the AAF 02/07 audit together with the strong level of service provided by Aviva during the COVID-19 pandemic. Aviva gave the Trustees updates on performance and of developments on a weekly basis through the initial phase of the pandemic and at frequent intervals since.

The Trustees and Aviva have agreed new reporting formats and management information during the Scheme Year and refined the SLA targets for administration and incorporated additional measurement metrics. Headline percentages of tasks within SLAs ran between 90% and 78% during the Scheme Year. The Trustees assessed the split between various types of administration tasks and noted good prioritisation of key tasks. Percentage calls answered, end to end times and Net Promoter scores are also monitored. These remained relatively stable through the start of the COVID-19 crisis at the end of the Scheme Year. At the height of the pandemic SLAs were running at 78% and end to end times at 14 days. Overall, the Trustees have experienced consistent, very good administration through the Scheme Year with problems reported and addressed by Aviva.

7. Communications – Trustee Assessment: Good – Aviva continues to enhance communications in accordance with the Scheme’s communications plan. The suite of communications is assessed as of good quality and comprehensive – although there are areas for development and in particular in the part of the member journey for the years immediately leading up to expected retirement. The Trustees now have even closer links with the Aviva marketing department, with an established review and approval process built into the Trustee terms of engagement, on their overall communications and engagement strategy. The Trustees and Aviva have considered how they can provide assistance to support the increase in member engagement and plans are in place to carry out further surveys with a focus on gaining further insight into members' views of the Scheme. As part of the newly developed Trustee Strategic Objectives, member communications have been highlighted as a key area of focus for the coming 12 months.

8. Member Journey Support – Trustee Assessment: Good – Support throughout the member journey is available to members through various channels, with Flexi Access Drawdown, Annuities and Lump Sum payments all available, continued work being developed to increase Scheme member engagement through direct marketing, and continued digital workplace proposition advancement using My Aviva being proposed for 2021. As part of the newly developed Trustee Strategic Objectives the member journey has been highlighted as a key area of focus for the coming 12 months.

The Trustees recognise that it is important that members understand how costs and charges can affect the amount in their pension pot. To help members do this the Trustees have produced a broad range of illustrations which show the effect that costs and charges and different investment returns could have on member pension savings. The Trustees have chosen to illustrate a representative sample of the funds available to members of the Scheme and in doing so have paid appropriate regard to statutory guidance. These illustrations are shown within Annex 3 of this Statement. Individual members benefit statements will show the web address for illustrations for the default investment options and other representative funds for their Employer’s Section of the Scheme.

Each Trustee of the Scheme is required by law to have a working knowledge of the Scheme’s Trust Deed and Rules, Statement of Investment Principles, and current policies for the administration of the Scheme. In addition, each Trustee must have an appropriate level of knowledge and understanding of pensions and trust law and investment principles. The purpose of these requirements is to ensure that the knowledge and understanding of each Trustee and the combined Board of Trustees is such that, together with the advice available to them, they can appropriately exercise their functions as Trustees of the Scheme.

The Trustees themselves have considerable relevant experience and expertise. Each of the Trustees have worked within UK pensions in various capacities for a considerable length of time and have a broad set of skills and wide general pensions knowledge.

In addition, each of the Trustees has a specialist pensions background with skills and knowledge which complement each other and provide a diversity of experience on the Trustee Board.

The Trustees are chosen to ensure that there is, collectively between them and with the input from Aviva and external advisers, the right balance of skills, knowledge and competencies to govern the Scheme effectively as well as an ability to challenge both Aviva and each other.

In August 2019, the existing Trustees of the Aviva Master Trust were adjudged as meeting the fit and proper test as set out by the Pensions Regulator as part of the Master Trust authorisation process. This involved a detailed analysis of the Trustees’ skills, knowledge and understanding and experience.

Elizabeth Renshaw-Ames and Tilly Ross joined the Scheme’s Trustee Board on 11 May 2020 following an extensive recruitment process (set out below). Elizabeth was also appointed Chair and Colin Richardson stepped down as Chair (remaining a Trustee). Elizabeth and Tilly submitted the necessary fit and proper documentation to the Pensions Regulator to demonstrate their skills, knowledge and understanding and experience.

A summary of the Trustees’ backgrounds is set out below:

PTL, represented by Colin Richardson. PTL is a specialist provider of independent governance services that acts as an independent Trustee on a variety of trust-based pension schemes. Colin is a qualified actuary and previously worked for a number of pension benefit consultancies. Colin also sits on governance committees for contract-based arrangements (including as the Chair of the Independent Governance Committee for Aviva) and holds the Pensions Management Institute Trustee Certificate. Colin is also a member of the Pension and Lifetime Savings Association Defined Benefit Council and the Pensions Regulator’s working party for standards of professional trusteeship. Colin is an Accredited Member of the Association of Professional Pension Trustees.

Rebecca Cooke. Rebecca’s background is legal having been a solicitor in private practice for over 30 years where she advised Trustees and employers on a full range of pension issues and with a specific interest in Trustee governance and pensions for not for profit organisations. She began her role with the Scheme in 2015 and, having left private practice in 2018, continued the trusteeship in a personal and independent capacity. Rebecca has a detailed knowledge of the Aviva processes and structures. She works closely with a number of different teams within Aviva to understand and bring focus to the needs of the Scheme. Rebecca also acts as Trustee of another medium sized master trust which is currently winding up having decided not to seek authorisation from the Pensions Regulator.

Jonathan Parker. Jonathan has worked in the workplace pensions and savings industry for over 20 years. He is currently Head of DC and Financial Well-Being at Redington as well as being Trustee of the Scheme. Prior to these roles, Jonathan held senior positions in insurance, consulting and asset management. Jonathan is an investment specialist and has worked with trustees and DC providers to design strategies suitable for their membership’s needs. He is a CFA® charterholder.

Anne Hunt (resigned as Trustee with effect from 11 May 2020). Anne has over 25 years’ experience of managing and administering both Defined Benefit (DB) and Defined Contribution (DC) Schemes and retired from her role as Pensions & Risk Benefits Manager at Warburtons in 2016 to focus on her role as independent Trustee. Whilst at Warburtons, the scheme was recognised by the pensions industry for the quality of its member communications. Anne has been a member of the Pensions and Lifetime Savings Association DC Council amongst other roles.

Elizabeth Renshaw-Ames (joined as Trustee with effect from 11 May 2020). Elizabeth has worked in the workplace pensions and savings industry for over 20 years. She is the current non-executive Chair of Barnett Waddingham LLP’s Management Board and was formerly Trustee CEO of the HSBC UK pension scheme. Elizabeth was also previously a Senior Partner at an Employee Benefit Consultancy. She is a Fellow of the Institute of Chartered Accountants in England and Wales and has significant expertise in governance consulting and has held consulting leadership roles in the UK and globally.

Tilly Ross (joined as Trustee with effect from 11 May 2020). Tilly is a qualified actuary and pensions professional. She was a Non-Executive Director of the Pensions Regulator up to end April 2020, is Independent Chair of Electricity Pensions Ltd and a former independent member of the Independent Governance Committee of Lloyds Banking Insurance. Tilly was previously Global Head of Pensions at National Grid PLC, responsible for managing the large defined benefit and defined contribution pensions schemes and trustee relationships and has over 25 years prior consulting experience.

In addition to their own knowledge, understanding and skills, the Trustees obtain support and advice from a range of sources, including from Aviva, two firms of legal advisers, an AAF auditor and firms of investment consultants. By providing bespoke advice and training relevant to matters relating to the Scheme at the appropriate times during the Scheme Year, this support has helped to ensure that the Trustees have exercised their functions as Trustees of the Scheme effectively.

As indicated above, two new Trustee appointments were made in May 2020. In accordance with regulations and the Scheme’s Trustee Selection and Removal policy, an open and transparent process was initiated during the Scheme Year for the recruitment of the two new Trustees. In order to increase the access to high calibre potential candidates, a recruitment search agency was utilised.

A number of considerations were incorporated in the construction of a Role Profile for the recruitment of the 2 Trustees. These included:

The following 3 Core Requirements of key areas of experience and specialism were identified as being important to the success to the Trustee Board:

During the Scheme Year, the appointment and interview process took place with the final appointment being made after the end of the Scheme Year. In combination, the two new Trustees, Elizabeth Renshaw-Ames and Tilly Ross provided the best experience and specialism described within these 3 Core Requirements for the needs of the Scheme.

The Trustees recognise the importance of training and development as part of their ability to continue to exercise their function as Trustees of the Scheme effectively. The Trustees ensure they have effective oversight of their training and development needs by operating their Trustee competency and effectiveness policy. The Trustees generally take the following steps to ensure that they carry out training and development activities that are appropriate to their functions in relation to the Scheme and ensure they continue to satisfy the legal requirements for Trustee knowledge and understanding:

Additional training needs relating to the areas set out below were identified during the Scheme Year and the Trustees are considering how best to address these going forward:

The Trustees’ policy on the selection of Trustees requires that each new Trustee carries out a thorough and appropriate induction programme to ensure that the Trustee can acquire a working knowledge of key Scheme documents and a sufficient knowledge and understanding of pensions and trust law and investment principles as soon as possible following appointment. The extent of the induction programme will depend on the skills, knowledge and competencies of the new Trustee. As a minimum a new Trustee will be expected to:

The Trustee toolkit is an online learning programme aimed at Trustees of occupational pension schemes. It contains modules and resources on the law relating to pensions and trusts, and the principles relating to the investment of occupational pension schemes. It is designed to help Trustees meet the minimum level of knowledge and understanding required under the Pensions Act 2004.

The Trustees completed the Trustee toolkit (or completed their latest update) on the following dates:

To support the appointment of Elizabeth Renshaw-Ames and Tilly Ross as new Trustees, an extensive Induction Programme was completed following the Scheme Year end covering the aspects listed above. This involved meetings with the other Trustees, the Scheme Secretariat, the Scheme’s Advisers, the Aviva Master Trust Governance Team and other key personnel from within Aviva.

The Trustees are satisfied that the Trustee training and development activities, knowledge and skills assessment processes and induction programme together with the support provided by Aviva and the Trustees’ advisers described above have ensured that, during the Scheme Year, the Trustees have met the requirements of sections 247 and 248 of the Pension Act 2004 (requirements for knowledge and understanding) and that they are able to properly exercise their functions as Trustees.

The Trustees have considered how to encourage representations and feedback given the size and demographics of the membership and the number of different employers.

The following arrangements have been made to encourage members of the Scheme, or their representatives, to make their views on matters relating to the Scheme known to the Trustees.

In response to the increasing size and changing demographic and nature of the Scheme, during the Scheme Year the Trustees worked closely with Aviva to assess and initiate improvements to the Scheme’s overall communications and engagement plan. They also explored new ways to encourage members, or their representative, to make their views on matters relating to the Scheme known to the Trustees. This work involved commissioning independent research with member focus groups. As a result of this work, plans are now in place to seek further member and employer feedback through surveys.

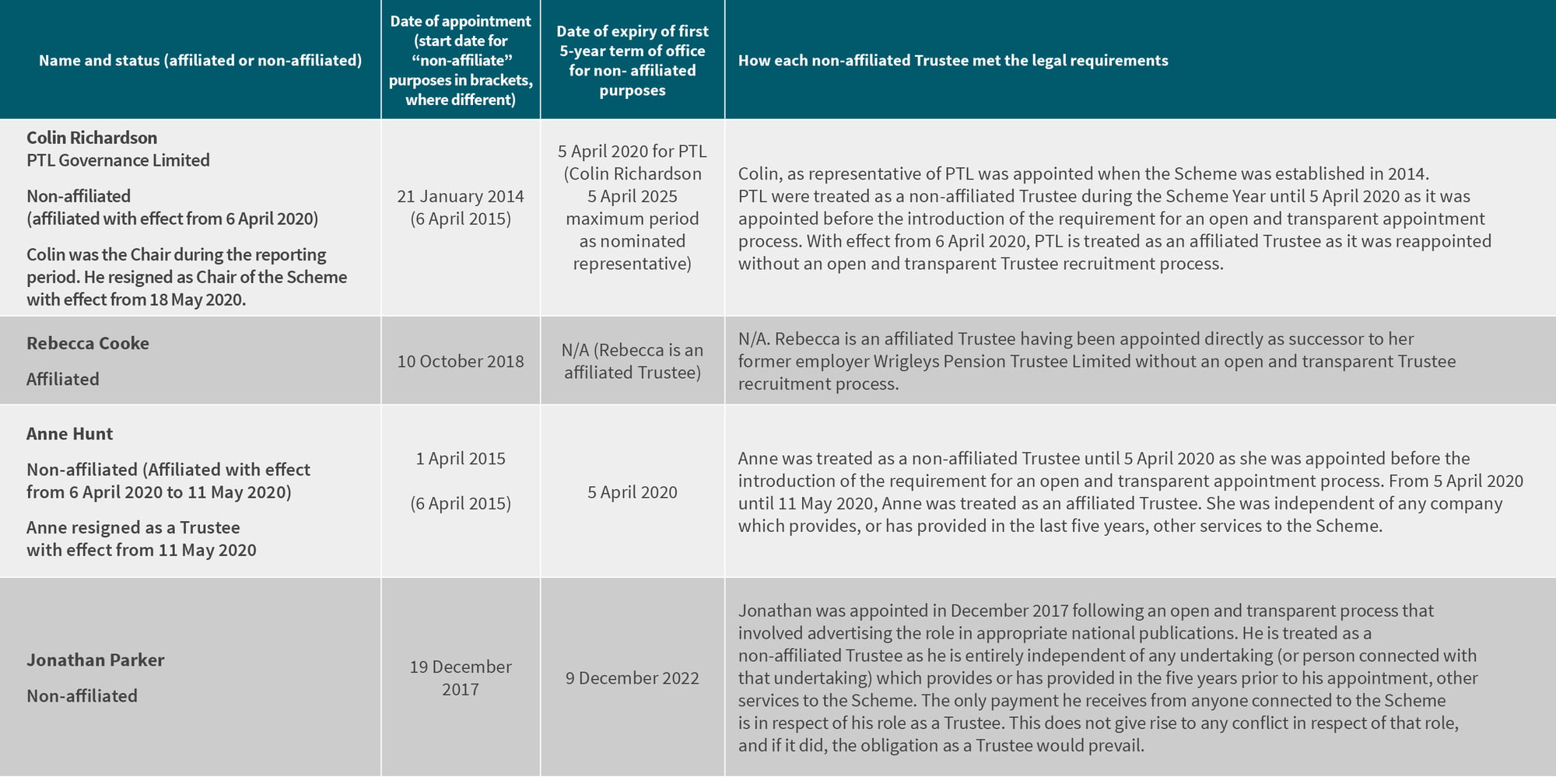

During the Scheme Year there were 4 Trustees, PTL represented by Colin Richardson (chair), Rebecca Cooke, Anne Hunt and Jonathan Parker.

On 11 May 2020, Anne Hunt resigned from the Trustee Board and was replaced by Elizabeth Renshaw-Ames and Tilly Ross.

On 18 May 2020, Elizabeth Renshaw-Ames was appointed as the new Chair of the Trustee Board.

As required by legislation, during the Scheme Year, the majority of the Trustees, including the Chair of Trustees, were non-affiliated with Aviva. For these purposes, “non-affiliated” means “independent of any undertaking which provides advisory, administration, investment or other services in respect of the relevant multi-employer Scheme”. There is also a requirement that any non-affiliated Trustees appointed after 5 April 2015 must have been appointed following an open and transparent process and that their terms of office must not exceed a specified length.

The table below shows which Trustees were affiliated and non-affiliated during the Scheme Year and how each of the non-affiliated Trustees met the relevant requirements. Following the end of the Scheme Year, there was a short period where the Scheme did not have a majority of non-affiliated Trustees and that PTL remained Chair whilst an affiliated trustee. However, legislation prescribes a 3 month period for this to be rectified. The appointment of Elizabeth and Tilly in May 2020 ensured compliance with the necessary legal requirements.

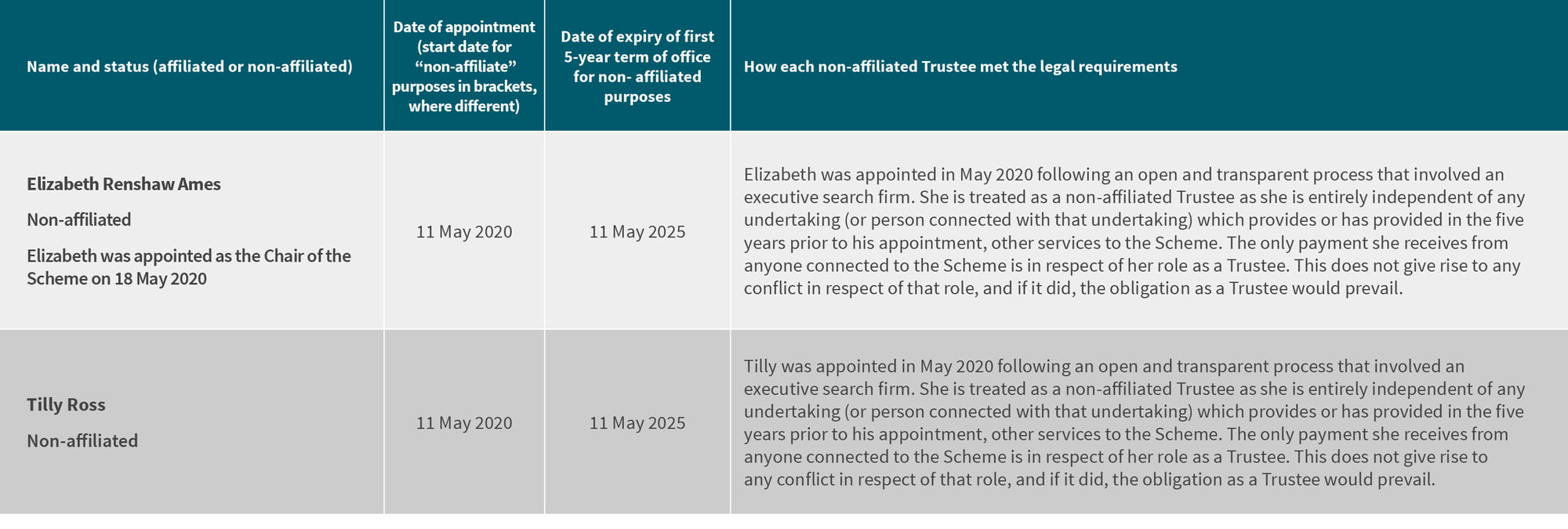

There were no new non-affiliated Trustees appointed during the Scheme Year. However, Elizabeth Renshaw-Ames and Tilly Ross were appointed as non-affiliated trustees on 11 May 2020.

The table below shows how Elizabeth and Tilly met the relevant requirements:

As described in Section 7 “encouraging representation from members”, all members are able to feedback directly through the member email address MTfeedback@aviva.com. Members can also contact the Trustees through their employers who are invited to attend forums to receive updated information and to provide feedback and ask questions.

Signed

Position: Chair of Trustee Board Name: Elizabeth Renshaw-Ames Date: 26 October 2020